$ASML Update

What price do we buy AI's permanent bottleneck

We had previously covered ASML in June 2025, when the markets were worried about revenue degrowth in 2026 due to Intel and memory manufacturers pulling back on capital expenditure and high revenue exposure from China.

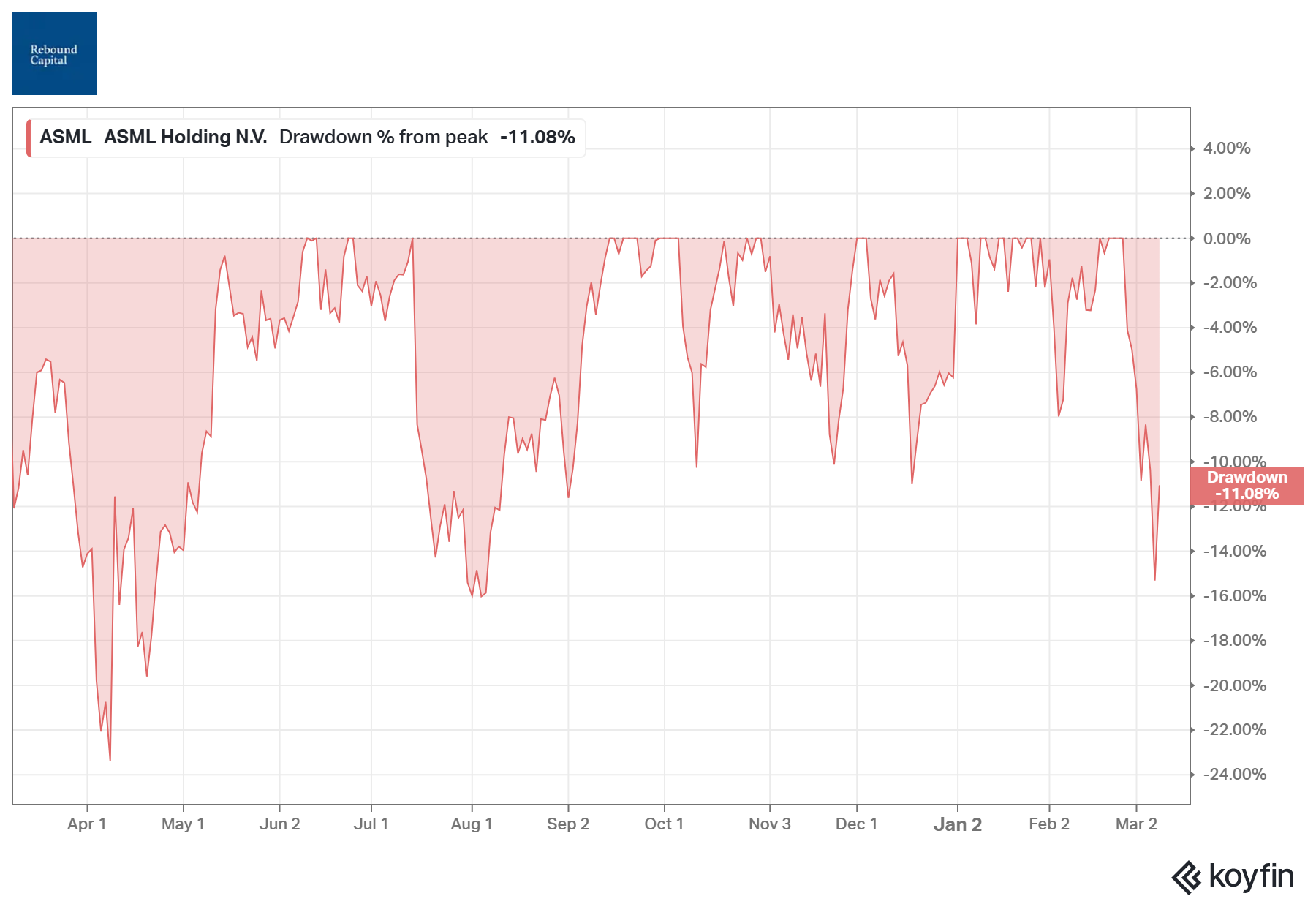

At that time, ASML was in a ~33% drawdown. Our thesis was simple. As the memory inventory clears and prices improve, memory manufacturers will start to reinvest in CapEx. On top of that, logic semiconductor sales will remain strong, and China’s revenue concentration will resolve itself in due time (and was a known risk). The stock is up ~70% since then. We never opened a position in ASML in June, despite a ‘Buy’ rating, since our portfolio was launched in August 2025.

With the stock down ~10% from its recent peak, a few of you reached out asking about our updated thesis on ASML. In this article, we will revisit our ASML thesis, focusing on ASML’s intrinsic value today and the price at which we would be comfortable buying ASML.

Reassessing the entry price for ASML

ASML remains a monopoly, and its competitive position is as strong as ever. In a world where AI will change all aspects of our lives, ASML is a key bottleneck for every leading-edge logic and memory chip produced worldwide.

Given the strong increase in capital expenditure guided by the Hyperscalers (Amazon, Google, Microsoft, Oracle) and Meta in 2026 vs. 2025, we update our internal valuation estimates for ASML and the key price levels at which we will enter the stock.

The trigger for this reassessment is the ~10% decline in ASML’s stock price (from the recent peak), partly due to heightened tensions in the Middle East. The stock has recovered, but we may get a second, deeper drawdown if the war continues longer than expected. Our simple analysis is that even though the US may want to end the war in the coming days, Iran may not want such an outcome: having already absorbed a lot of pain in the conflict, they will want to impose costs on the US - primarily through blocking the straits of Hormuz. Hence, the markets may drop again, offering an opportunity to buy ASML.

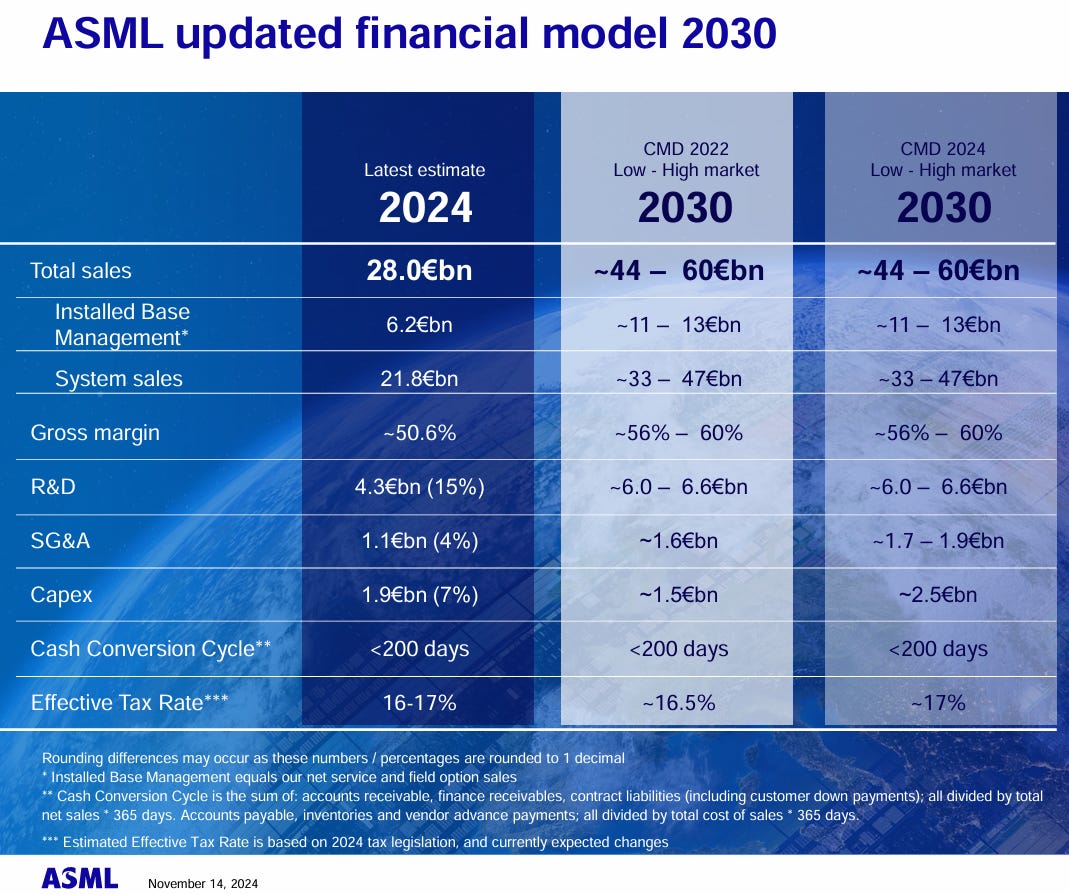

ASML 2030 Guidance

ASML has guided the following for the business in 2030:

We expect ASML to reach the upper end of its guidance in 2030. This is because capital expenditure on AI-enabled data centers has grown substantially since late 2024, when ASML issued the guidance above. We present a few graphs to show the scale of increase in capital investments (a material fraction of which will be used to buy ASML’s machines).

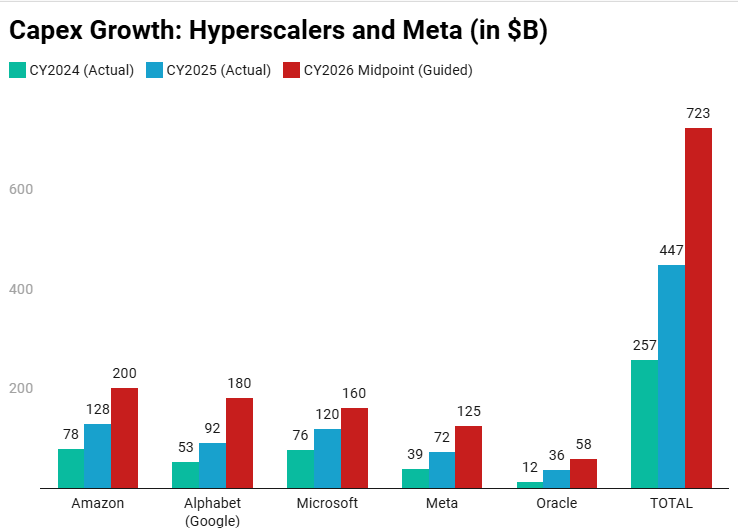

Hyperscalers’ capex growth

Capital expenditure by Hyperscalers and Meta is expected to grow by more than 40%-50% in 2026 vs. 2025. This capex is spent on buying logic and memory chips, both of which require ASML’s machines to produce.

ASML’s 2030 business model framework is very conservative. This is because it was given before the inflection point in AI usage, driven by applications like ChatGPT and Copilot, which went viral in 2025 and early 2026.

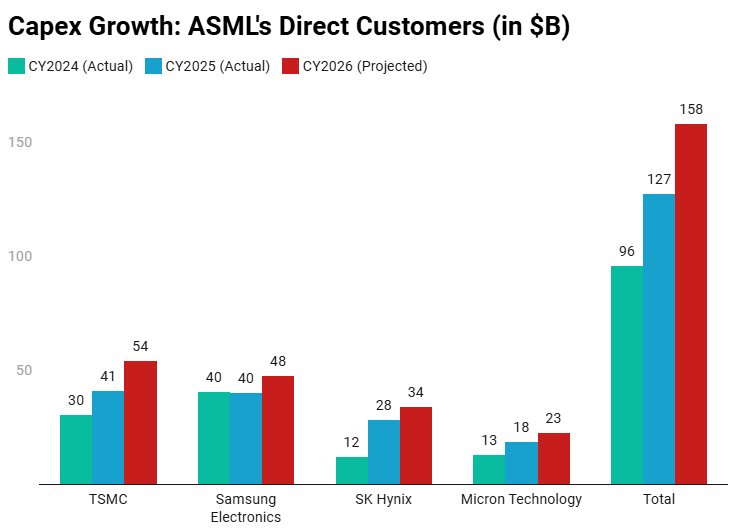

ASML’s customers’ capex growth

After analyzing the capex growth for the largest AI companies (whose capex indirectly flows to ASML), we will now compare the growth in capex for ASML’s largest direct customers - the logic and memory chip manufacturers. These companies are also ramping up capex in 2026, which will directly benefit ASML (ASML’s revenue is driven by its customers’ capex).

Given the strong increase in capex by ASML’s customers and the largest AI companies, we are confident that ASML will reach the higher end of its revenue guidance by 2030.