Deep Dive: Amazon (Updated)

Will AI Capex deliver good ROI?

We are publishing this Amazon update without a paywall

Quick recap before we begin. In November, we bought Amazon at ~$236 with one simple claim: AWS isn’t losing the AI race. It was out of capacity. Growth would re-accelerate the moment new data centers came online.

In December, we doubled down on our thesis and made Amazon our largest position.

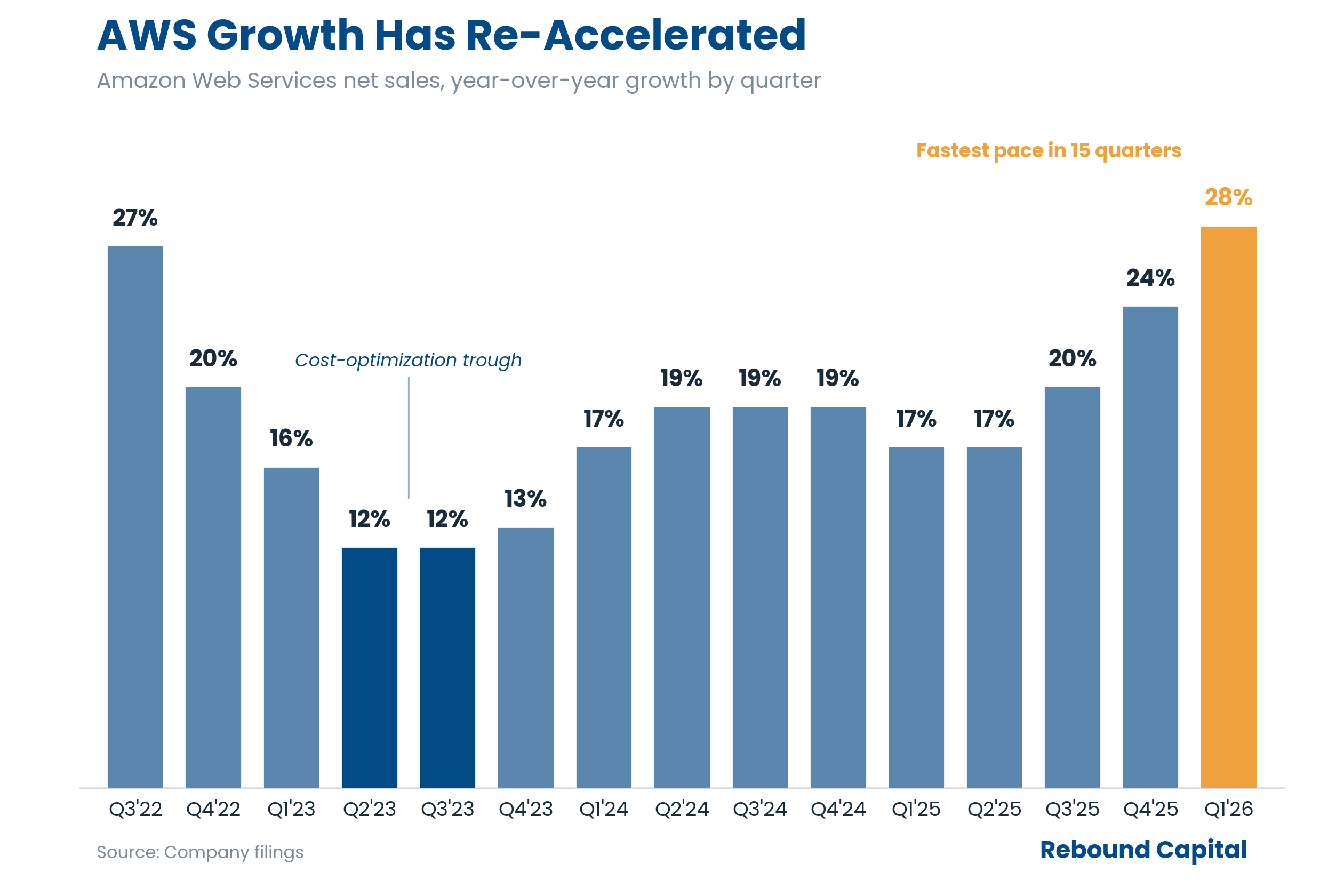

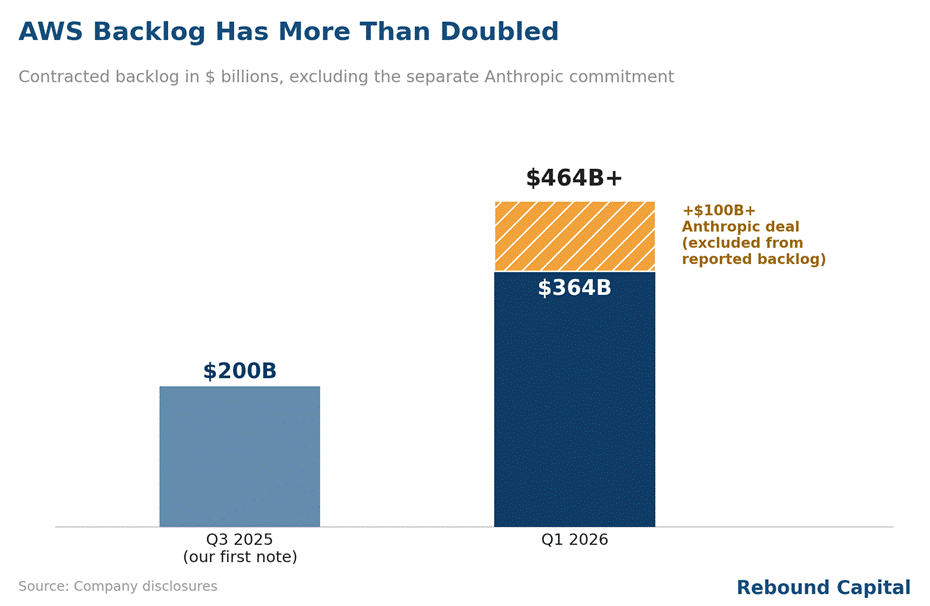

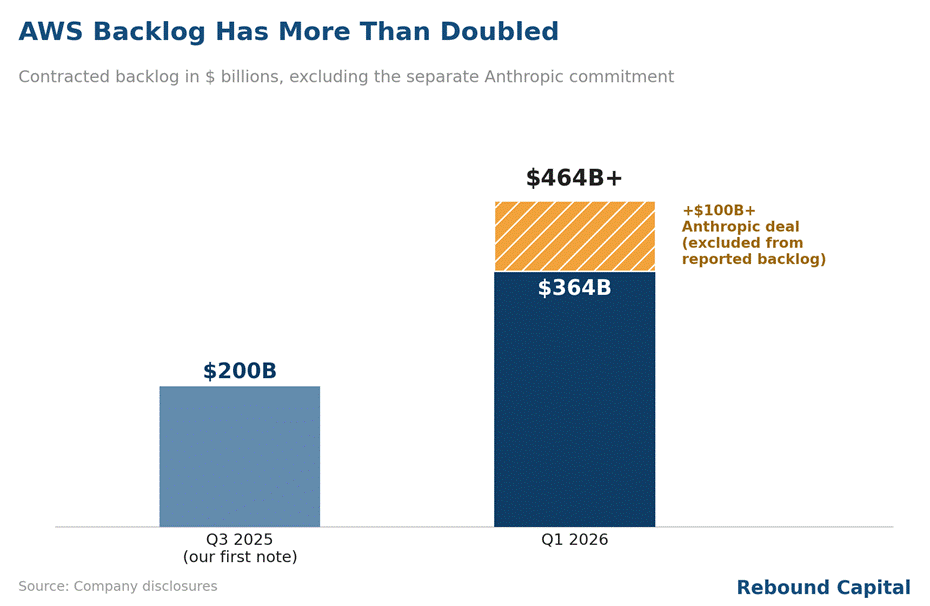

Two quarters later, AWS grew 28% YoY last quarter (its fastest pace in 15 quarters). The backlog has nearly doubled, and Amazon has built one of the largest custom-chip businesses in the world (Graviton, Trainium, and Nitro), worth ~$50B annually at external prices.

And the stock? Back to ~$245. Right around our entry. When we are right about the business and the stock goes nowhere, it’s usually a good time to re-check our thesis.

A year ago, the fear was that Amazon was losing cloud market share due to weak AI offerings. Today, the fear is that Amazon is doing well in the AI data center market, but this business itself is not attractive from an ROI perspective (Amazon has committed to spend up to $200B in CapEx this year). The market is worried that Amazon and other hyperscalers will trade like utilities in the future due to heavy capex, low pricing power, and little to no free cash flow for investors.

We think the market is wrong for the second time.

Before you proceed, we highly recommend reading our original thesis on Amazon, as well as our December follow-up.

Welcome to Rebound Capital. We study beaten-down stocks and businesses that have made successful comebacks. Subscribe for free to join our growing community of 23,100+ subscribers and make sure you don’t miss our next briefing.

We got the AWS thesis right

When we laid out this thesis in November, the overhang was specific: AWS was well regarded but widely seen as losing the AI race, ceding cloud share to Azure and GCP without a clear lead in foundation models or silicon. We took the other side, arguing that AWS, together with three underappreciated high-margin engines (Advertising, the 3P marketplace, and Prime), would drive the economics. Two quarters later, all four have accelerated.

AWS: grew 28% last quarter, its fastest in 15 quarters, vindicating our call that ~20% growth was due to supply issues. Backlog has reached $364 billion (before adding a separate $100 billion commitment from Anthropic).

Advertising: revenue crossed $70 billion in the trailing 12 months, still compounding above 20% (up from the >$60 billion we flagged in November), with margins better than most software businesses.

Silicon: the chips business (Trainium, Graviton, Nitro) has reached a $20 billion run rate, growing in the triple digits.

Subscription services (including Prime): revenue up 15% to an annualized ~$54 billion, with 15% worldwide unit growth, the fastest since Covid.

With the re-acceleration confirmed, the debate now centers on whether AWS will earn a decent ROI on $200 billion in annual capex. Our answer is yes. We will list 4 structural reasons the market is not pricing in. Let’s dig in.

The New Wall of Worry

On the February call, management guided to ~$200 billion of 2026 capex, roughly $54 billion above what the street had modeled. Shares slid from ~$240 to about $197 in about 10 days! The market feared that the AI buildout is outpacing demand and that years of record spending will yield an uncertain return.

The bears have two arguments why ROI on hyperscaler Capex will be poor:

Depreciation: hyperscalers assume GPUs have an economic life of 5 to 6 years, but bears argue the true economic life is closer to 2 or 3 years, overstating profits and free cash flow.

The counterparty question: what if the labs can't pay? The largest names driving the cloud backlog for hyperscalers are loss-making businesses that depend on continuous outside financing to honor multi-year contracts. OpenAI is estimated to have a ~$14 billion loss for 2026 with no free cash flow before the end of the decade; Anthropic is closer to breakeven but still burning capital. A backlog is only as good as its counterparty, and if funding for frontier labs tightens, a portion of that $364 billion (plus the $100 billion-plus Anthropic commitment) would be tied to companies that need to raise capital again to pay it.

We take both points seriously, but neither negates the thesis.

Regarding depreciation, the 2-3-year clock assumes a GPU is worthless once it is off the frontier (as newer GPUs have better compute per dollar). In practice the retirement decision is economic, not functional: an already-paid-for chip has near-zero remaining capital cost, so it stays in service as long as the inference revenue it earns beats its power and rack cost. Chips retired from training cascade into inference and other workloads that don't require the latest hardware, and Amazon's breadth of price-sensitive demand keeps that older silicon utilized rather than stranded, extending useful life and softening the write-down.

We watch the profitability of the LLM labs closely, and they seem to be trending well (with Anthropic rumored to be heading towards profitability), but it does not break the thesis because Amazon is selling infrastructure, not betting on who will succeed. If a lab stumbles, the workloads route (toward cheaper open-weight models that still run on AWS silicon, billed by AWS) rather than evaporate. The bear case requires the demand itself to be fake. It is not. What would genuinely concern us is a broad, simultaneous pullback in enterprise AI spending that neither open-source nor rerouting could absorb, and we see no evidence of that today.

Share this report with a friend

Key changes in AI that the market is overlooking

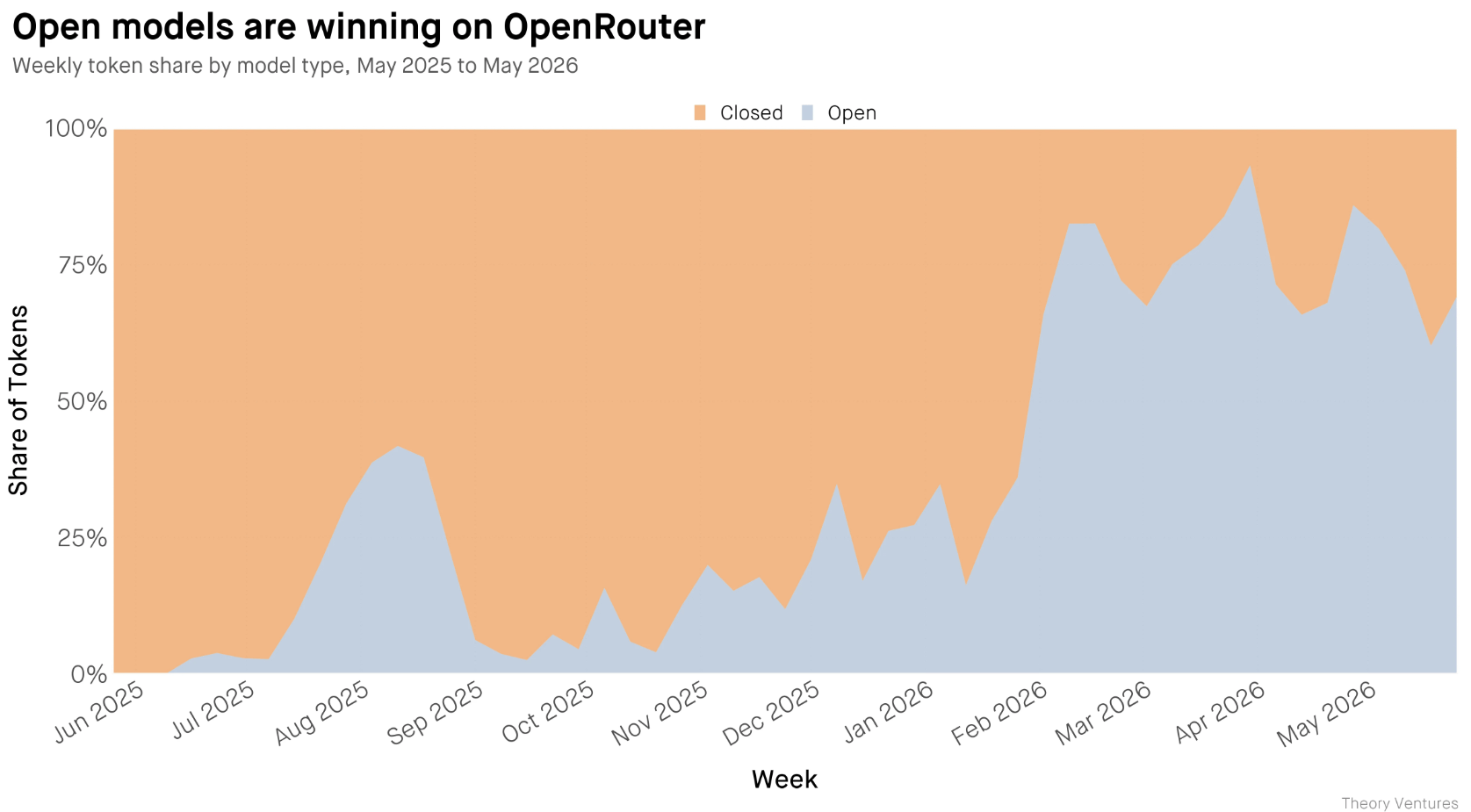

The rise of open source: orchestrators will keep a larger share of the pie

As open-source models become more capable and the gap to the leading models keeps narrowing, especially for the day-to-day, mundane tasks that fill most enterprise workloads, the LLM labs will lose pricing power. The value will then migrate to whoever orchestrates the workload. This will be the cloud companies, such as AWS, GCP, and Azure.

Think of payment networks. Merchants compete brutally on price. Brands rise and fall every decade. But the network in the middle clips every transaction at the same rate, no matter who wins.

In AI, the models are becoming the merchants. AWS (and other cloud companies) is the network. We are not saying that Anthropic's and OpenAI’s margins will be as low as we see for merchants. But this is a good illustration of how the value will shift.

Since ChatGPT was launched, enterprises pointed every workload at the best model on the leaderboard and ignored the bill. The bills have now arrived. For example, Uber reportedly burned through its 2026 AI budget in four months, then capped employees at $1,500/month for coding tools. Coinbase’s CEO laid out a step-by-step method by which his company reduced its AI spending while increasing its token usage.

The rational response is not to use less AI. It is to route the routine 80% of requests (classification, extraction, summaries, boilerplate code) to cheap open-weight models like DeepSeek, Qwen, Kimi, Llama, Nemotron, and only the genuinely hard 20% escalates to a frontier model. This is already happening and will accelerate.

Here is a good chart showing how much open-source model usage has increased.

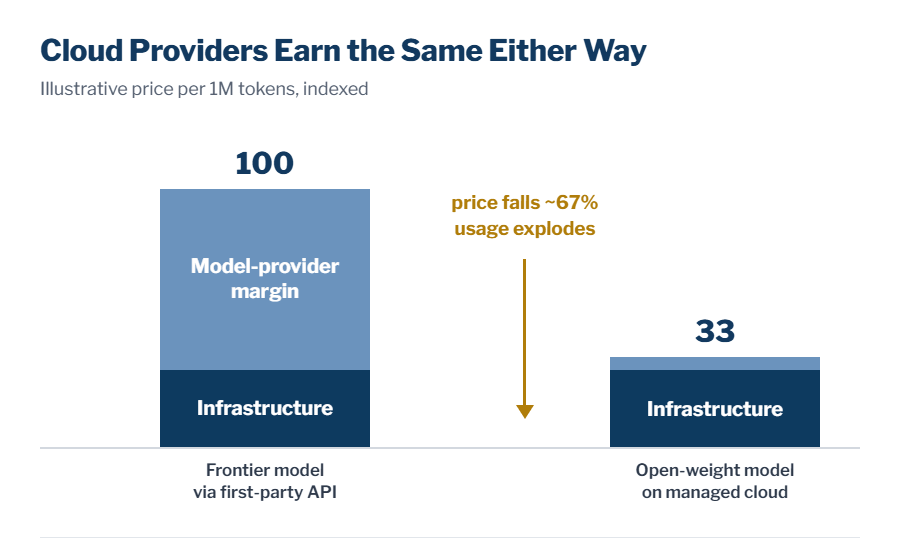

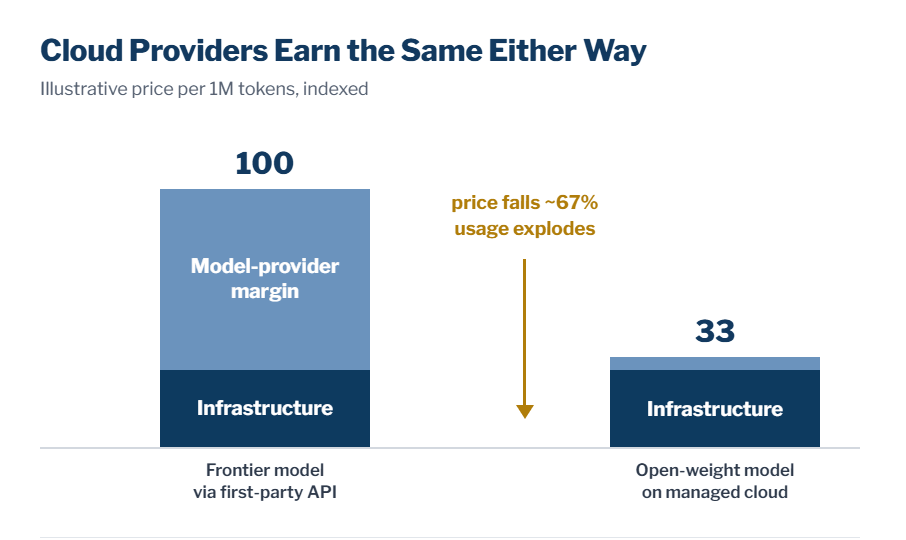

Routing reduces the model layer’s pricing power and increases the total TAM for cloud providers as usage explodes:

As the workload shifts from a frontier model to open-source models, model providers’ margins decline because many models are now ‘good-enough’ to handle most tasks. But the token still runs on someone’s chips and security architecture. That’s how the cloud providers will produce value.

Cheaper tokens don’t shrink usage. They multiply it. This means higher revenue for cloud providers that help enterprises deploy AI. The hyperscalers are investing in forward-deployed engineers for the same as well.

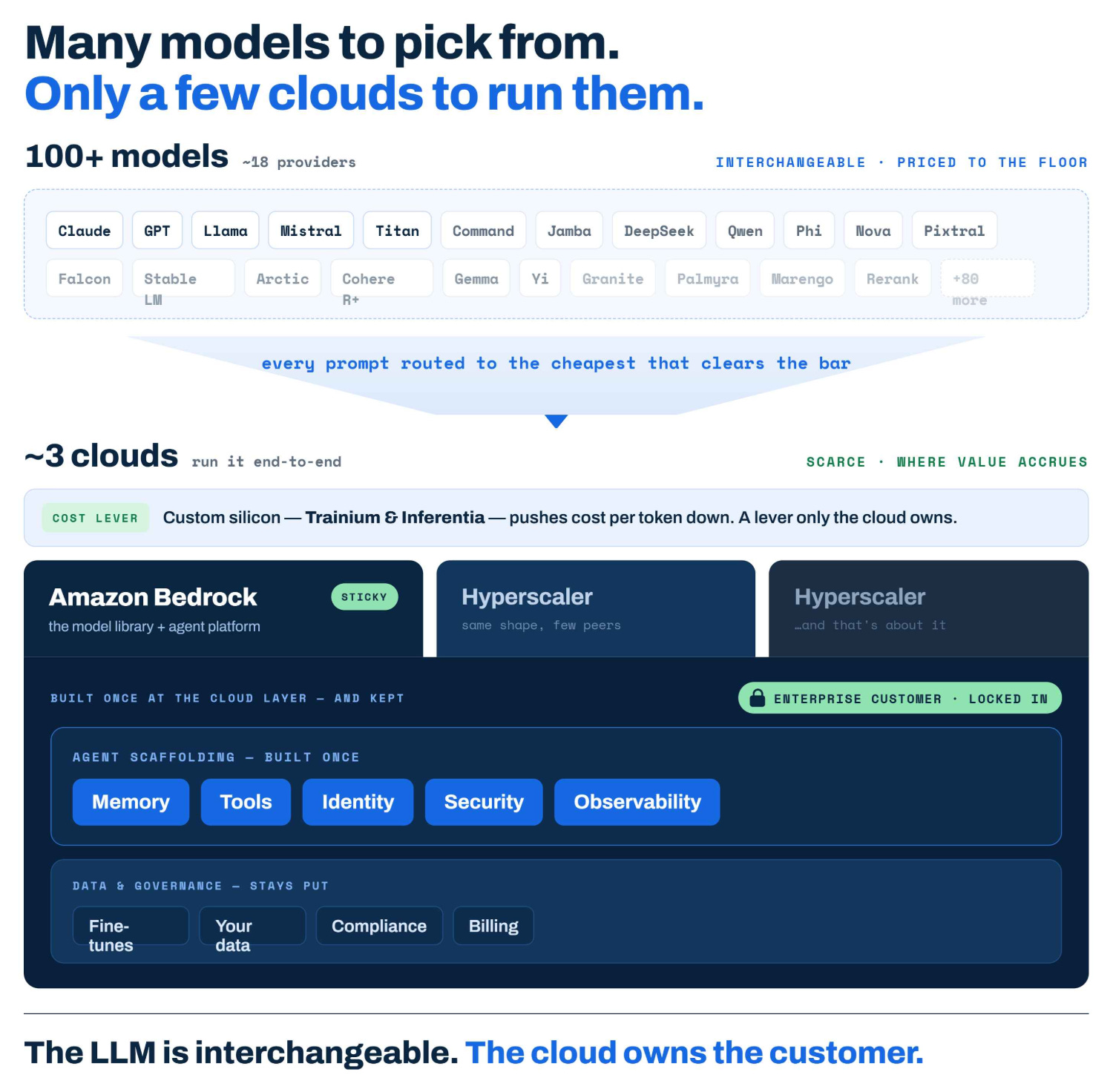

Switching costs are rising for cloud services and lowering for LLMs

As models become easy to swap, the cloud beneath them becomes harder to leave. Bedrock (AWS’s AI models library) hosts 100+ models from ~18 providers, can route prompts to cheaper models when they clear the quality bar, and provides the agent scaffolding (memory, tools, identity, observability) that an enterprise builds once and keeps. The fine-tuning, data, compliance, and billing all sit in the cloud layer, so switching models becomes a dropdown, not a migration. The lab is interchangeable. The cloud owns the customer.

June showed why no enterprise will want to rely on a single LLM lab. A new executive order creates a voluntary framework under which the most advanced models spend up to 30 days with the US government before wider release. Days later, Anthropic’s newest models were suspended worldwide for 19 days under an export-control directive. When model availability can change overnight, driven by a government decision, enterprises will want the option to route their workloads to different models and, ideally, use open-source models within the safe confines of a large cloud provider (which can ensure there is no backdoor data transfer and can host the model).

Slower than hoped expansion of data centers in the US

The key shortage in AI has shifted from chips to power, which favors whoever already has capacity in the ground. Interconnection queues in the markets hosting most of 2026’s announced capacity (Northern Virginia, Phoenix, Dallas) now run four to seven years, and of the ~16 gigawatts slated for the US in 2026, only about 5 are under construction, with ~11 stuck behind transformer, switchgear, and interconnection backlogs.

Amazon has the most capacity, locked in over years via nuclear offtake, its own substations, and ~$200 billion of 2026 capex. Every year the buildout runs slow, Amazon’s already-energized capacity grows more valuable, its pricing firmer, and its $364 billion backlog more defensible.

And even as those backlogs clear, a second barrier is coming up: community opposition. Sightline calls local resistance a material driver of project delays or cancellation. Maine has passed a statewide moratorium, and similar measures are moving in ten-plus states. That makes new sites harder to permit, which only widens Amazon’s edge.

Amazon’s successful internal custom ASICs

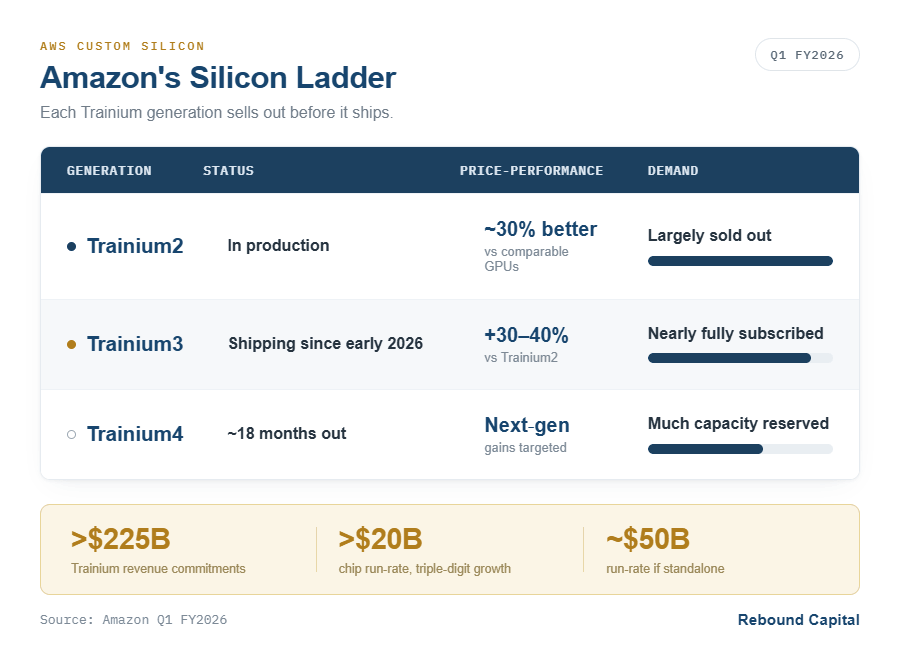

In a world where models commoditize, the lowest cost of compute is the moat. Designing your own chip is how one gets to the lowest cost. Trainium3, generally available since December, runs at roughly 4x the performance of Trainium2 and about 50% lower cost than GPU alternatives. The custom-chip portfolio (Trainium, Graviton, Nitro) has crossed a $20 billion run rate, growing triple digits.

The demand is strong: most Bedrock inference runs on Trainium today, Trainium2 is effectively sold out, and Trainium3 is nearly subscribed, anchored by Anthropic’s 5-gigawatt and OpenAI’s ~2-gigawatt commitments. AWS is vertically integrated: every dollar of inference on Amazon’s own chip is margin that Nvidia does not earn. That is the key to the open-source shift. As routine tokens move to good-enough models, whoever owns the cheapest chip will get the most workloads, and increasingly that chip is Amazon’s.

Why is Amazon our leading choice rather than Azure/GCP?

Fair question, since Microsoft and Google also have cloud businesses. The difference is that both compete with the LLM labs, whereas Amazon does not:

Google wants Gemini to win the race for the best LLM model. It directly competes with Anthropic and OpenAI. This means that the leading labs will not want to give Google too much of their cloud business (unless the compute constraints are too strong).

Microsoft is not neutral either. It owns roughly 27% of OpenAI and is now building its own MAI models to cut its AI bill, so its economics tilt toward specific models winning rather than staying indifferent across all of them. Microsoft competes directly with Anthropic and OpenAI for productivity software.

Amazon is the only one of the three without its own frontier model in the race, which is exactly what allows Bedrock to act as a neutral router. It has no model whose success it needs to defend, so it can send each workload to whatever wins on price and quality. (The natural objection is Amazon's stake in the labs, but Amazon now backs both leading names, not one. It led OpenAI's $122 billion March round with a $50 billion commitment, bundled with two gigawatts of Trainium and AWS as the exclusive third-party cloud for OpenAI's enterprise platform. Amazon is not betting on a winner. Amazon is ensuring its cloud platform is used irrespective of who wins.)

To be precise, Amazon does build models. Its Nova family exists, but it is a cost lever, not a must-win. Google and Microsoft need a specific model to win because their economics are tied to Gemini and to winning in productivity software. Amazon does not. Whether Nova wins or loses, the tokens still run on AWS, on Amazon's chips, billed by Amazon.

That neutrality is important as it prevents any conflict of interest for the LLM labs. Amazon’s AI business rides on compute infrastructure, not model IP, so it does not need to back the right lab:

If the frontier labs keep winning, the tokens run on AWS.

If open source wins, the tokens still run on AWS (AWS will prefer this scenario).

If any single lab stumbles, Amazon is selling the cloud beneath all of them rather than being caught out on one bet.

Key Risks

The risk is simple: we are wrong about demand and the margins AWS will earn. Amazon will spend ~$200 billion this year on data centers, chips, and power. This spend will not deliver good returns if AWS’s operating margins reduce from current levels. If the demand fails to materialize (we are confident that this won’t happen), then, again, the CapEx would have been ill-timed and would need time to digest.

The following key risks materializing would change our view:

AWS growth back below 25% for two consecutive quarters. In fact, we expect AWS growth to exceed 30% in the coming quarters.

AWS’s operating margins reduce in the coming quarters

The backlog stalls, or Trainium slips a generation against Nvidia’s roadmap.

AWS raises Capex without giving further data to show customer commitments against which it is raising capex. Or if it doesn’t communicate clear ROI on the $200B in spending (at least in theory).

Amazon Valuation

Our base case puts Amazon’s intrinsic value at ~$310, about 25% above its current price. The build runs to 2035, discounted at 8%, and rests on four things:

Third-party seller services compound in the double digits early and fade toward 6%, growing from ~$172 billion to nearly $400 billion.

Advertising, now a >$70 billion business still growing north of 20%, roughly doubles over five years as retail media and video keep scaling.

AWS decelerates from the 28% it just printed toward the high teens by 2030, then to ~10% by 2035. Even fading, it roughly triples this decade and carries about two-thirds of company profit by 2030.

Operating margin climbs from ~11% to ~17% by 2030 as the mix tilts toward the high-margin engines and automation deepens.

Access our full model here:

Rebound Capital Rates Amazon a ‘Buy’

Amazon stays our largest position in the Rebound Portfolio. We hold a full position, so we are not adding here, and we will look to trim as the stock approaches our ~$310 base case.

Two honest observations. We hold a full position from ~$236, so this is not a fresh buy. At ~$247, the ~25% upside to fair value meets the margin of safety we require, and we are content to sit and let the business close the gap.

The bull case values Amazon near ~$487, close to a double from here. The bear case puts Amazon at ~$184, a roughly 25% drawdown. In this scenario, the multiple is down modestly and we assume AWS growth and margins disappoint. It does not assume the business breaks. The downside is a dented compounder, not a broken one.

A decade ago, cloud was a sliver of IT budgets. Add inference, agents, and the wholesale re-platforming of enterprise software onto that base, and the runway runs to the trillions. AWS enters that race in the lead, with the installed base, the power, and now the silicon to serve it at a lower cost than anyone else. Open source is commoditizing Amazon’s suppliers, model makers, and merchant chip vendors, not Amazon. It only widens the moat around the company that owns the rails.

Rebound Capital’s work is provided for informational purposes only and should not be construed as legal, business, investment, or tax advice. You should always do your own research.