Deep Dive: Microsoft ($MSFT)

Too cheap to ignore?

Microsoft has dominated enterprise software for the past 30+ years and consistently reinvented itself through different waves of technological change. Read our primer on Microsoft to learn more about its foundation and how Mr. Nadella completely changed Microsoft’s fortunes after taking over as CEO in 2014. Another recommended read on Microsoft’s history is this article by Quartr.

along with major milestones in each era.")

The investment thesis for Microsoft has undergone a fundamental transformation over the last 2-3 years, shifting from a software-as-a-service (SaaS) model to a vertically integrated, capital-intensive artificial intelligence provider (Azure).

Welcome to Rebound Capital. If you are new here, we conduct in-depth research on beaten-down stocks and study companies that have made successful comebacks. Subscribe for free and join 21,300 other investors to make sure you don’t miss our next briefing.

Today, Microsoft is a combination of a defensive, high-margin software provider (potentially under threat from AI) and a capital-intensive infrastructure play that is essential to the global economy’s digital transformation. We will dig into Microsoft’s revenue model, the hyperscale cloud industry, and the intrinsic value of its shares.

Why is it down?

As of March 2026, Microsoft (MSFT) is trading roughly 33% below its October 2025 peak of $555. This correction has erased nearly $1.3 trillion in market value, driven by a shift from AI enthusiasm to a demand for concrete financial returns.

The downturn is primarily attributed to three factors:

The ROI Gap: Investors are growing wary of massive capital expenditures. In the most recent quarter, Microsoft’s CapEx surged 66% to $37.5 billion. The market is now penalizing this spend, demanding proof that these multi-billion-dollar data center investments will deliver decent ROI.

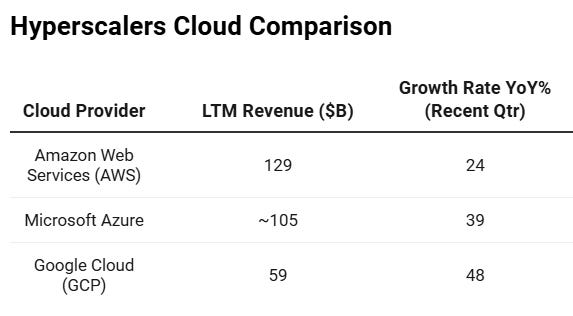

Decelerating Azure Growth: While still robust, Azure’s year-over-year growth slowed from 40% to 39% (with forward guidance of 37%). In a high-valuation environment, even a 1% deceleration signals to investors that the cloud market may be reaching a temporary saturation point.

OpenAI Concentration Risk: Approximately 45% of Microsoft’s $625 billion contract backlog is currently tied to OpenAI. Analysts have flagged this as a significant counterparty risk, questioning the stability of a backlog that is so heavily dependent on a single, unprofitable partner.

Microsoft in the AI Era

In 2023, Microsoft was off to a great start with generative AI. They bought a material stake in OpenAI and leapfrogged their rivals to become the face of AI. They integrated AI into their search engine, Bing, and rumors surfaced that they were taking market share from Google.

Cut to 2026, Microsoft has not released any popular AI product. Their partnership with OpenAI has had its share of problems, and their most successful division in the last decade, Azure, is now transitioning to a very capital-intensive business model, with uncertain ROI. Anthropic’s productivity software releases, such as its Excel and PowerPoint plugins, have threatened Microsoft’s core productivity business.

On top of that, the competition in the cloud business is so intense that Amazon and Google are guiding to nearly $200B of CapEx in 2026, with Microsoft’s trajectory pointing towards >$150B in CapEx. Investors are rightfully worried about this level of expenditure.

This pressure on its core moat, combined with the capital-intensive nature of its cloud business, has led to the stock dropping by more than 30%. Microsoft was once looked at as a beneficiary of AI, but not anymore. There are serious concerns about Microsoft’s ability to compete in an AI-first world.

Business segments

Productivity and Business Processes (PBP)

This segment is the backbone of the modern workplace. It includes the Office 365 suite (Word, Excel, Teams with >300 million users), LinkedIn, and Dynamics 365 (Microsoft’s ERP and CRM software). PBP is Microsoft’s most profitable division, with operating margins exceeding 60%. In the last 12 months, PBP has generated approximately $125B in revenue and $78B in operating profit.

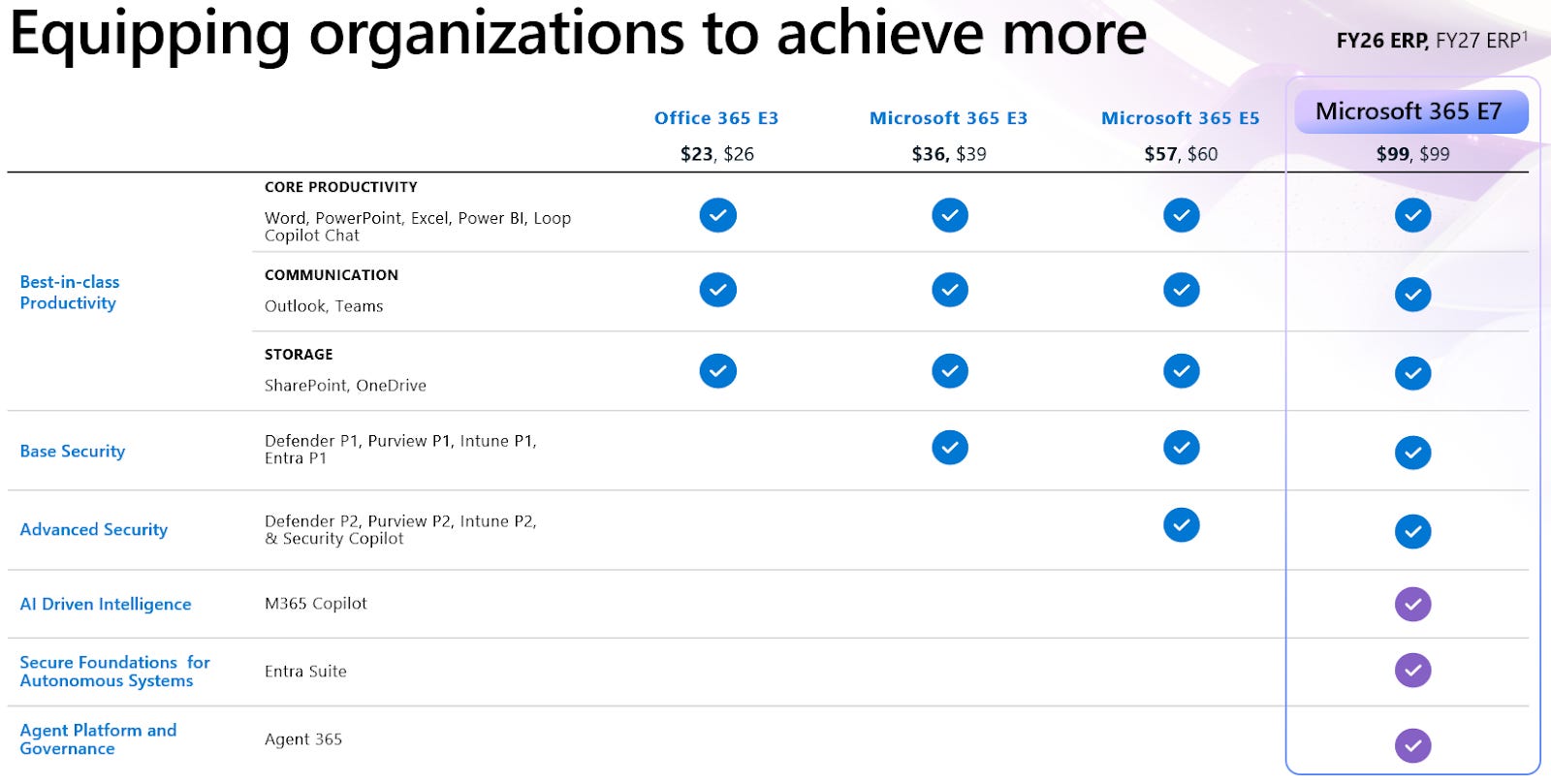

Within Microsoft 365 Commercial, the installed base has reached approximately 450 million seats. While total seat growth has moderated to mid-single digits (6%-7% YoY), revenue growth is increasingly driven by a ‘mix shift’ towards premium licensing tiers. The transition from Office 365 E3 to E5 represents a significant ARPU uplift, as the E5 ($57 per user per month) tier includes advanced security, compliance, and analytics, and is priced around 60% higher than E3 ($36 per user per month). The Microsoft 365 E7 suite will be priced at $99 per user per month and will be available from May 1, 2026. The E7 suite will provide users access to Microsoft’s latest agentic AI tools and the latest Copilot.

Another key product in the PBP segment is LinkedIn. It has continued to grow as the leading global professional network with >1 billion members. Revenue growth is ~10% and is driven by a mix of premium subscriptions, talent solutions, and advertising. LinkedIn is integrating AI to automate hiring workflows and personalize ad targeting, helping maintain higher engagement amid a broader hiring slowdown.

The key investor concerns for the PBP segment center around Microsoft’s inability to develop popular AI productivity tools. Microsoft reports 15 million users of Microsoft Copilot. But, is this $30/month add-on actually being used, or is it shelfware bundled by Microsoft? Claude’s Excel and PPT add-ins are more popular than Microsoft’s own Copilot.

The second headwind concerns seat-based software sales. If agents replace knowledge workers, how will Microsoft transition to a value-based model that charges for productivity gains or outcomes rather than for features? How does this transition affect Microsoft’s margins? Will MSFT be dependent on the foundation model owners, and how will this affect its profitability?

It is quite instructive how well-received Anthropic’s Excel and PowerPoint add-ins are. Whether Microsoft will be able to continue growing revenue at high rates in PBP will depend on its ability to deliver value to users. The upcoming E7 launch is critical. More on that later.

Intelligent Cloud

Intelligent Cloud includes Azure (Microsoft’s cloud division), GitHub, and server products (Windows Server, SQL Server). It has generated $122B in revenue over the last 12 months. In the most recent quarter, its revenue grew by 29% YoY, with Azure growing at 39% YoY. This segment has an RPO (remaining performance obligations) of $625B, signaling strong future revenue visibility. However, 45% of this is tied to OpenAI, exposing Microsoft to vendor-concentration risk.

The key debate regarding the IC segment is whether Microsoft (and other cloud providers) will be able to derive sufficient ROI from their mammoth investments in their cloud computing divisions. The Hyperscalers have indicated approximately $660B in capital expenditures in 2026, primarily for their cloud divisions. Paradoxically, Microsoft is currently capacity-constrained, and management highlighted that they had to prioritize spending on internal products, which slowed Azure growth.

Industry Structure and Evolution of Cloud

The cloud infrastructure and enterprise software industries have entered a phase of extreme concentration. The landscape is now dominated by Microsoft (Azure), Amazon (AWS), and Alphabet (GCP). In 2018, these big 3 held ~55% of the global cloud infrastructure market. By 2025, this has increased to 68%. This consolidation is driven by an astronomical barrier to entry: these 3 companies spent a combined $260B in CapEx in 2025 alone. This effectively means that very few companies can compete in this space (In fact, very few countries can match this level of CapEx!). We are in a land-grab phase, with the final ROI of the massive AI investments uncertain. But with 3 companies competing, we expect the industry to deliver decent ROI for investors in the coming years. We expect the market’s fears about high cloud capex to subside in the coming quarters as revenue from monetizing AI begins to be recognized.

More Personal Computing

This is the legacy segment covering Windows OEM, devices, gaming, and search (Bing). Its LTM revenue is $55B, and in the most recent quarter, the segment’s revenue contracted by 3% (primarily due to weakness in Xbox hardware sales).

This segment is much smaller than the other 2 and is not expected to grow much. Hence, its performance will not decide the fate of Microsoft’s stock. We will focus on the other 2 segments for the remainder of the article.

Microsoft vs Amazon vs Alphabet

A key question is why Microsoft trades at a lower multiple than Amazon and Google. In 2025, Microsoft generally traded at a premium relative to Google and Amazon. So, why the flip now?