Deep Dive: Netflix ($NFLX)

A masterclass in pricing power

In 2000, a struggling DVD-by-mail company flew to Dallas and offered to sell itself to Blockbuster for $50 million. Blockbuster's chief executive reportedly laughed the idea out of the room. That little company was Netflix. Today, Blockbuster is down to a single store in Bend, Oregon, while Netflix has rewired how the world watches television and stands as the undisputed leader of streaming.

But by late 2025, Netflix was the one chasing legacy content. In December 2025, it agreed to buy Warner Bros. Discovery’s studios and streaming business for roughly $83 billion. The disruptor was now trying to become a consolidator.

The market did not like it. 2 things spooked investors: the roughly $59 billion of debt the deal would require, and the suspicion that this merger was being done to mask slowing organic growth. The deal finally fell through. Netflix was outbid by Paramount. The stock rose ~40% over a couple of months after this news, then gave back most of the gains. It now trades ~$81, down nearly 40% from a 52-week high of $134.

In January, we put Netflix in the too-hard bucket. We said we would revisit it once the merger was resolved or the multiple came down. Both have now happened. We sense an opportunity here.

The market has taken a maturing growth narrative, layered on AI fears (AI-generated content and short-form video eating into engagement), and event risk (the abandoned Warner Bros. bid and Reed Hastings leaving the board), and marked the multiple down.

What it has underestimated is Netflix’s strong free cash flow generation. Trading at ~3.3% NTM FCF yield, Netflix offers a rare combination of double-digit earnings growth and a mature level of cash generation, supporting continued buybacks and shareholder returns. With the advertising engine just beginning to gain momentum, FCF can grow at a mid-teens CAGR over the coming 3-5 years. This is not a demanding valuation, given that Netflix is a market leader and will continue to compound for many years.

How Netflix makes money

Netflix reports a single segment, but earns revenue from two distinct businesses. The first is the subscription business: about 325 million paid memberships at the end of 2025, monetized through a tiered pricing ladder. The second is advertising, still small but scaling fast. We model the two separately. Subscriptions are an annuity. Advertising is a high-margin opportunity where Netflix can leverage the platform it has built over 20 years and the nearly one billion people it now reaches.

Welcome to Rebound Capital. We study beaten-down stocks and businesses that have made successful comebacks. Subscribe for free to join our growing community of 22,400+ subscribers and make sure you don’t miss our next briefing.

The core subscription segment

This segment earns revenue through subscriptions. Here, Revenue = (no. of subscribers * average revenue per subscriber). Several critical levers drive subscriptions:

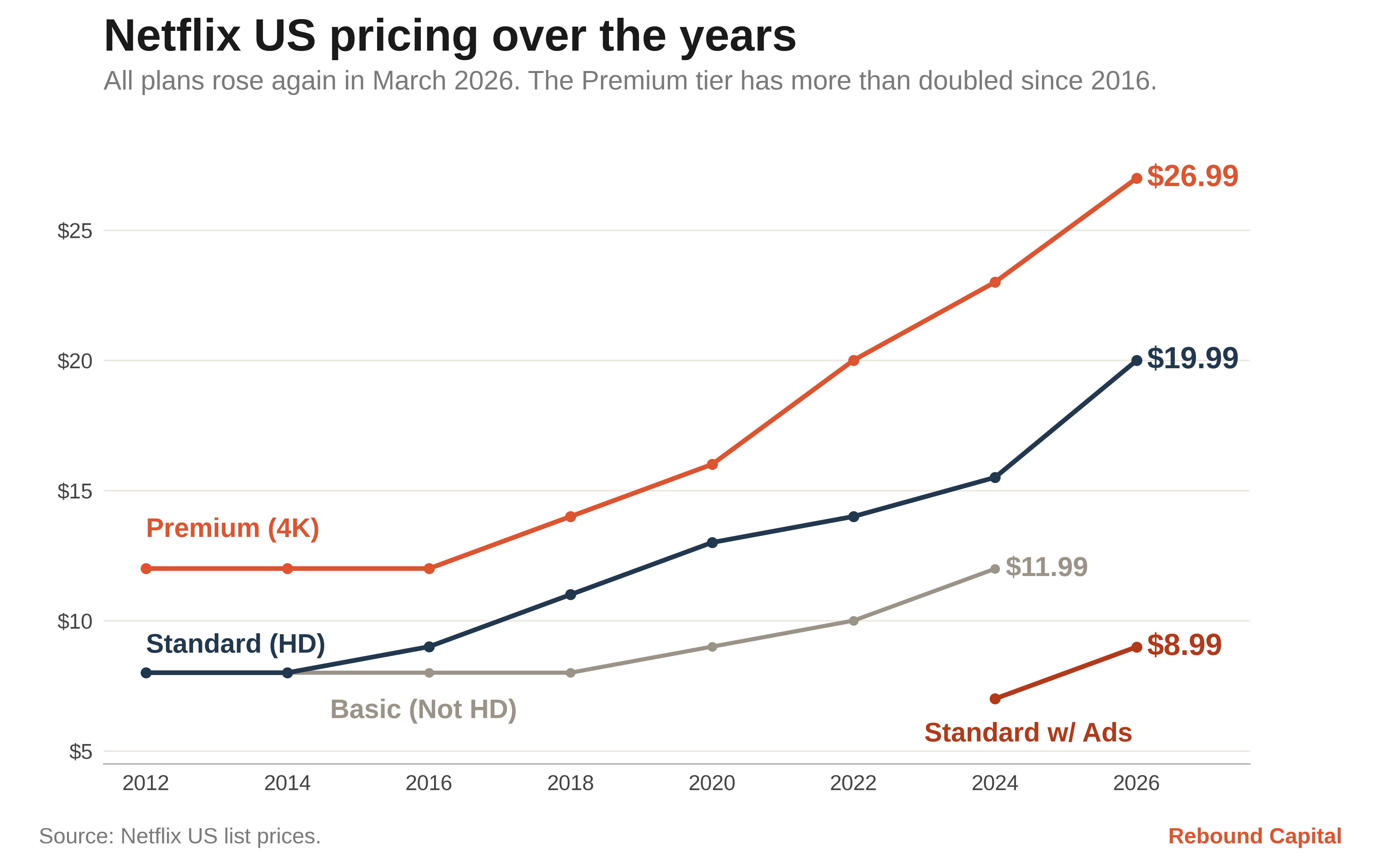

Pricing power: Netflix pushed through a US price increase in March 2026, and year-over-year retention improved across all regions during the cycle. This proves Netflix’s strong pricing power. The US Standard plan has climbed from $7.99 in 2011 to $19.99 in March 2026, roughly a 150% increase, while adding hundreds of millions of members along the way. The latest March 2026 move lifted all three tiers by an average of about 11%. Independent analysts at JPMorgan pegged the annualized revenue uplift at roughly $1.7bn and flagged minimal churn risk.

Category-leading retention: Data from Antenna indicates Netflix has the lowest churn in the category, generally under 2% per month, compared with a premium-SVOD average of 4% to 5%. When a household decides to trim its streaming bill, we think Netflix is typically the last subscription to go, not the first. This structural habit creates a powerful lock-in effect.

The advertising segment

The ad tier has reached more than 250mm monthly active viewers by May 2026, up from 190 million in November and just 94 million in 2024. Ad revenue grew more than 2.5x in 2025 to over $1.5bn and is guided to roughly double to $3bn in 2026, with an internal ambition (leaked documents) of nearly $9bn by 2030. Most of that is incremental, high-margin revenue on content that already exists. We think the internal target may prove to be conservative.

In-house ad stack transition: Netflix has built its own first-party platform, the Netflix Ads Suite, and finished rolling it out across all of its ad markets in 2025, moving away from rented Microsoft systems. It now transacts programmatically through Amazon DSP, Yahoo DSP, The Trade Desk, and Google DV360, with >50% of impressions bought programmatically.

Netflix uses AI to build ad creatives matched to specific shows, with brands reporting significantly better execution. It has layered on AI media-planning tools, generative pause and interactive formats. The advertiser count has crossed 4,000, up about 70% year over year. Premium streaming commands premium CPMs (cost per 1000 views), and Netflix already sits at the top of the stack. It draws some of the highest ad rates in streaming, roughly $30 to $40 per thousand impressions, ahead of mid-tier peers like Hulu and Disney+. The edge is structural, with premium content, a light ad load of 4-5 minutes per hour, and scarce inventory that advertisers compete for. Pair that pricing power with the largest audience in streaming, and the ad business has a long runway.

Advertisers’ Feedback: To check if Netflix’s ad platform is working, we look at 2 different data points:

Highest CPMs in the streaming industry.

Netflix’s own data: at its May 2026 Upfront, it claimed campaigns run almost twice the TV norm for brand building and 23% above purchase-intent benchmarks, with 44% of its ad audience not reached elsewhere on TV.

The more important signal is the revenue growth in advertising (2.5x in 2025 and 2x in 2026), and on the Q1 2026 call, the advertiser count crossed 4,000, up about 70% year over year, with programmatic nearing half of non-live sales. That is a vote cast with real money.

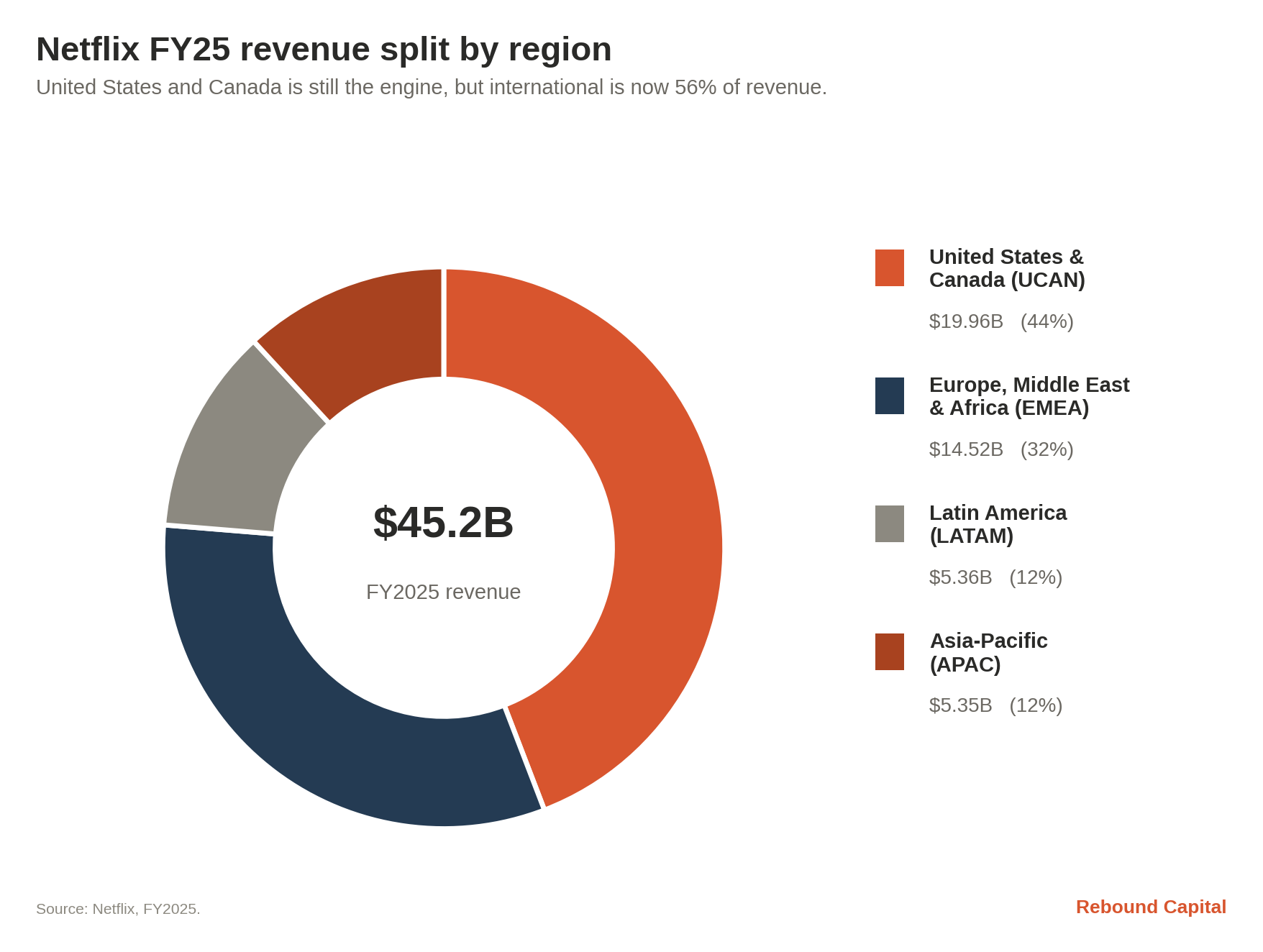

Geographic Distribution: UCAN, EMEA, APAC, and LATAM

US and Canada (UCAN): The largest region, at roughly $20bn revenue, actually reaccelerated to mid-teens growth as price increases flowed through. This region can compound at rates in the high single-digit to low double-digit range in the coming years.

Europe, the Middle East, and Africa (EMEA): Now nearly a third of revenue at about $14.5bn, this region grew in the high teens in Q1’2026.

Asia-Pacific (APAC): This is the fastest-growing engine, compounding at ~20% (in 2025), driven by India, Japan, South Korea, and Southeast Asia.

Latin America (LATAM): The most price-sensitive region grew in the high single digits on a reported basis, but constant-currency growth was roughly 30% in 2025. The drag there is due to currency translation, not customer demand.

We estimate that only the US, Canada, and Europe are close to being saturated. The rest of the regions can support a mid-single-digit to low-double-digit CAGR in subscribers till 2030.

What Went Wrong

The current drawdown in Netflix from its June 2025 high near $134 to around $81 (a ~40% decline) is driven by a fundamental narrative shift: the market has derated Netflix, fearing disruption from AI-generated content and maturing markets.

Growth metric anxiety: Netflix stopped disclosing paid subscriber counts and churn at the start of 2025, leaving the market anxious about slowing headline net adds and shifting visibility.

The engagement plateau: Short-form video content on YouTube and TikTok is competing for attention and capping engagement growth, with growth slowing to roughly 2% in H2 2025. Digital i’s measurement shows average daily use per Netflix account slipped from 101 minutes to 93 minutes, while YouTube account use rose to 99 minutes, indicating real cannibalization of hours.

Generative AI structural fears: Bears worry that generative AI will flood the world with cheap synthetic video content and erode the long-term value of a premium owned-and-licensed library.

Headline noise: Headline and event risks have weighed heavily on sentiment, including the abandoned $83bn Warner Bros. bid and Reed Hastings's leaving the board in June 2026.

Netflix’s Competitive Moat

Netflix’s moat is a system of interlocking competitive advantages - each reinforcing the others and proving highly resilient to the current environment.