Deep Dive: Wingstop ($WING)

A franchise royalty platform with software-like margins

In 1994, Antonio Swad and Bernadette Fiaschetti opened a wing shop in a strip mall in Garland, Texas. The idea that a restaurant brand built around twelve sauces and a small fryer might one day list on NASDAQ and compound more than 20x off its IPO price at its peak would have struck almost anyone in the chicken business as absurd.

32 years later, Wingstop has 3,153 restaurants. Around 98% of the system is operated by franchisees - what the company calls ‘brand partners’. The company had 21 consecutive years of positive domestic same-store sales (2003-2024). Wingstop keeps the brand IP, the flavors, the technology platform, and a 6% royalty on every dollar of system sales, while taking on almost none of the operational complexity. This is an amazing business model, akin to Domino’s Pizza.

The brand partners are very happy too. Brand partner unit-level cash-on-cash returns are >50% for a ~$575,000-$650,000 buildout. The payback period is close to 2 years for most partners! No wonder Wingstop has a pipeline of 2,200+ committed restaurants, even in a weak consumer environment.

But the stock is down ~65% from its all-time high.

Welcome to Rebound Capital. We study beaten-down stocks and businesses that have made successful comebacks. Subscribe for free to join our growing community of 21,900 subscribers and make sure you don’t miss our next briefing.

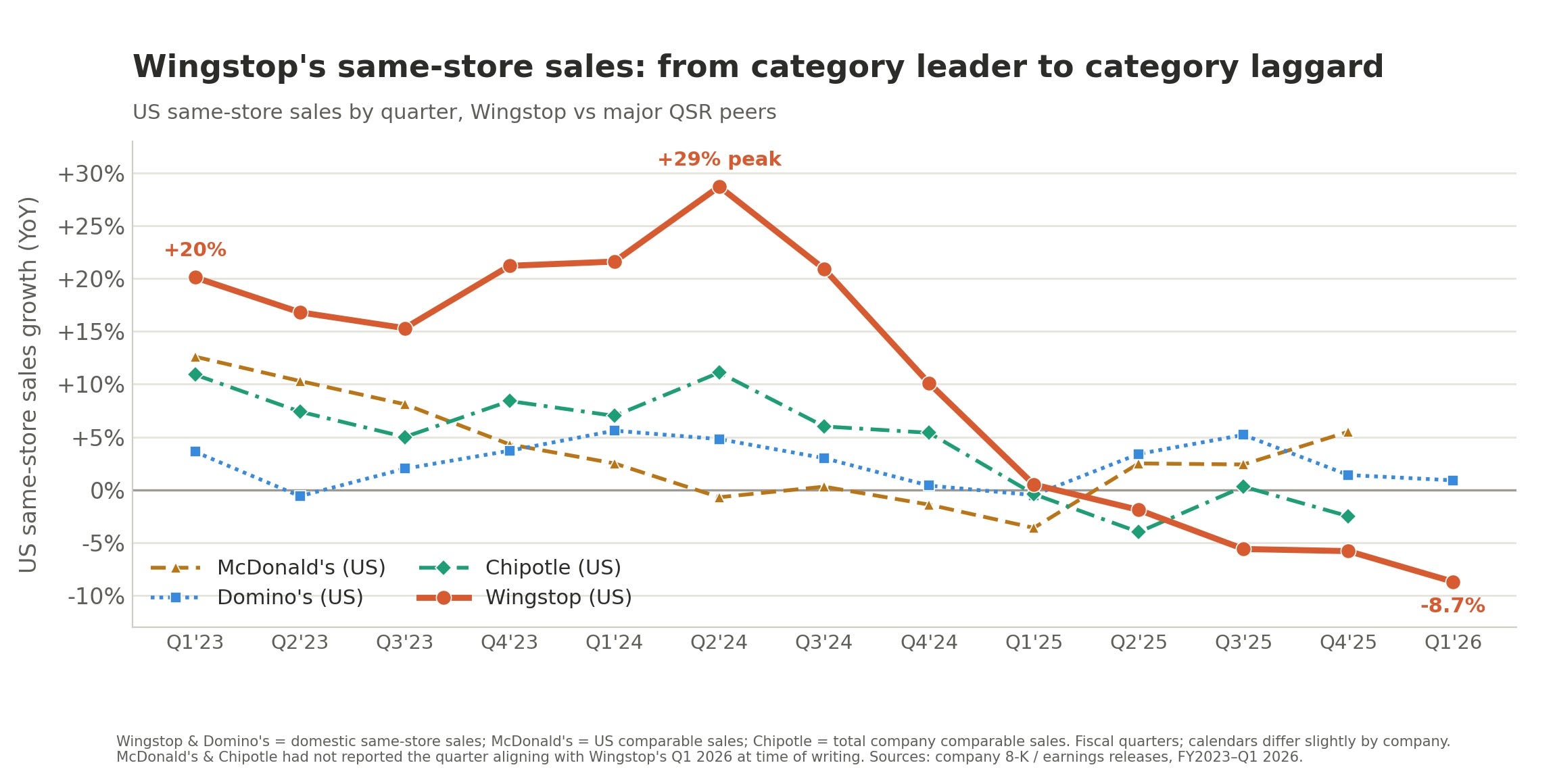

The drawdown is due to the 2025-26 deceleration in domestic same-store sales growth (SSSG%). SSSG% fell to (-3.3%) in fiscal 2025 (the first negative year since 2002). Q1 2026 was worse at -8.7%. The franchise royalty engine, by contrast, is not broken, and brand partners are still investing to open Wingstop stores (over 2,000 restaurants in the pipeline). The debate isn't whether Wingstop is a great business; it is. The debate is whether a great business trading at ~23x EBITDA, with its core customer under pressure (and weak consumer sentiment more broadly), is a buy today.

How Wingstop makes money

I would say that Wingstop is not really a restaurant company. This is a company that owns IP and a brand, which it licenses at very high operating margins, and it operates 3 businesses under that brand.

Royalties

Wingstop gives out franchise rights to its partners. These ‘brand partners’ then pay a 6% royalty on every dollar of domestic system sales (& 5% on international sales), plus franchise fees, technology fees, and rebates. Wingstop does not deal with food costs, labor, rent, or working capital. Wingstop has ~1,335 corporate employees versus 3,153 restaurants. Corporate complexity scales sublinearly, while royalty revenue scales linearly with system sales. FY2025 royalty/franchise/other revenue was ~$322M, with an estimated ~40% operating margin (excluding the marketing revenue, which is a pass-through). This revenue segment is what makes Wingstop an elite business.

The advertising fund

Brand partners contribute 5.5% of sales to a national advertising fund. This is a near-perfect pass-through - fees in, advertising expenses out, with a zero economic margin to corporate. The strategic value is the scale. A 5,000-store system contributes more dollars to the same Super Bowl spot than a 3,000-store system. It is a brand-building utility, not a margin business.

Company-owned restaurants

Wingstop owns 57 corporate stores, mostly in the Dallas Fort Worth area, generating ~$128M of sales at ~24% restaurant-level margin. This is small in absolute dollars, but strategic. Every new operating standard, technology platform, and menu innovation gets tested here first. Corporate AUVs (Average Unit Volume: sales in a year) are tracking toward $2.5M, a $500K premium over the system average, and serve as a proof point of what disciplined operations produce.

Wingstop is a royalty platform selling its IP and brand, an advertising fund, and a small laboratory of company-owned restaurants. The royalty segment is what creates the economic value. The other 2 segments are used to maintain the brand's vibrancy.

Unit economics

I will dig into the unit economics for both the brand partners and the corporate/company (which we will enjoy as investors).

Franchisee economics: A Wingstop franchisee typically spends $575,000 to $650,000 to build a single location. In return, the store generates roughly $2 million in annual sales while maintaining a 22% to 25% restaurant-level profit margin - allowing owners to recover their initial investment in just 2 years. These metrics represent some of the strongest unit economics in the Quick Service Restaurant (QSR) industry. This rapid payback is driven by a comparatively smaller restaurant size - locations average just 1,400 to 1,700 square feet, completely bypassing costly drive-thrus and large dining rooms to focus entirely on takeout and delivery. Ultimately, these elite-operator returns are driving explosive brand growth for Wingstop. As an operator, why choose any other brand when Wingstop delivers such stellar returns? This is a significant moat.

Company economics: The corporate economics are stellar. They are even better than the headline numbers. Wingstop reported a 25.7% operating margin on FY2025 revenue of $697M, except that about $248M of that ‘revenue’ is just the advertising fund passing through the P&L (fees in, ads out, no economic margin). Strip it out, and the real operating margin on the business Wingstop actually keeps is closer to 40%!

Why is it down 65%?

5 factors explain the move from $420+ in mid 2024 to $157 today:

Same-store sales broke a 21-year positive streak: Domestic SSSG went from +19.9% (2024) to -3.3% (2025) to -8.7% (Q1 2026). Consumer distress has played a large part in this. It’s difficult to say when the consumer will bounce back, though management expects a bounce back in the second half of 2026.

Multiple compression as growth slowed: At the mid-2024 peak, the stock traded above 40x EV/EBITDA, a multiple that only made sense against 20%+ same-store sales growth. As that growth turned negative, the market re-rated it toward a more normal ~23x (LTM). That compression accounts for ~50% of the decline, and it occurred only because of the slowing growth.

Q1 2026 one-time shocks: Atypical winter weather temporarily closed 700+ restaurants in January. Then, the Middle East conflict pushed gas prices higher. Finally, the lower-income cohort is in consumer distress and spending less.

Repeated downward guidance cuts damaged management's credibility: Wingstop entered 2025 guiding to low to mid single-digit domestic same-store sales growth. After Q1, it cut that to roughly 1%. After Q3, it cut again, this time to a 3-4% decline. Due to these frequent cuts, the market has stopped paying for the medium-term targets, including the $3M AUV goal, until they are proven.

Secular fears about GLP-1 drugs: The longer-term effects of GLP-1 drugs on eating out are inconsistent, but many reports highlight a lower propensity to eat out (as we highlighted in our Domino’s Deep Dive). But still, there is now a strong possibility that eating out may be structurally inhibited by people consuming GLP-1 drugs. Mind you, these drugs can keep getting better, and so the full effect is still largely unknown.

These factors are correlated, not independent. None permanently impairs the underlying business engine, but a few of these can be long-term headwinds to growth.

Competition and International Expansion

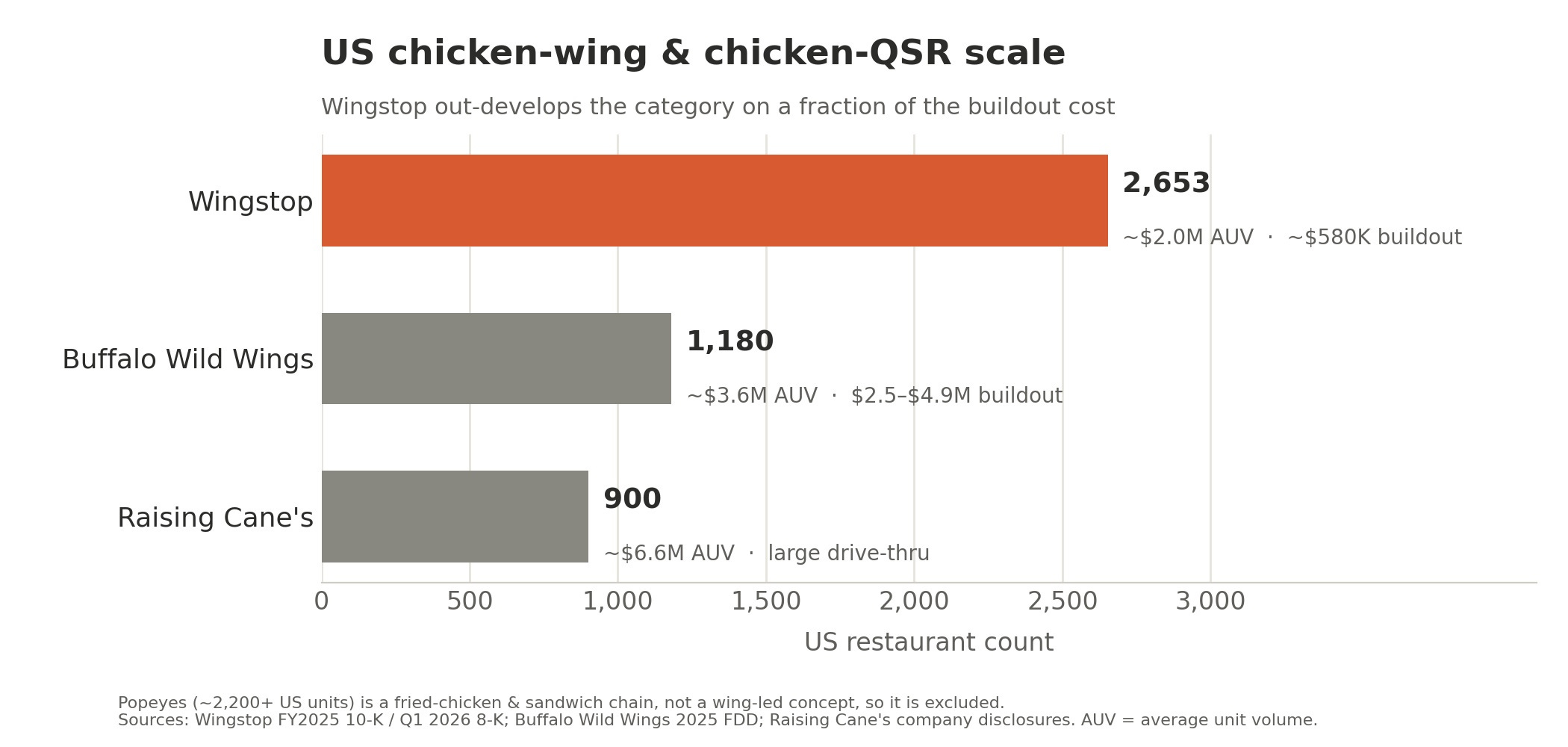

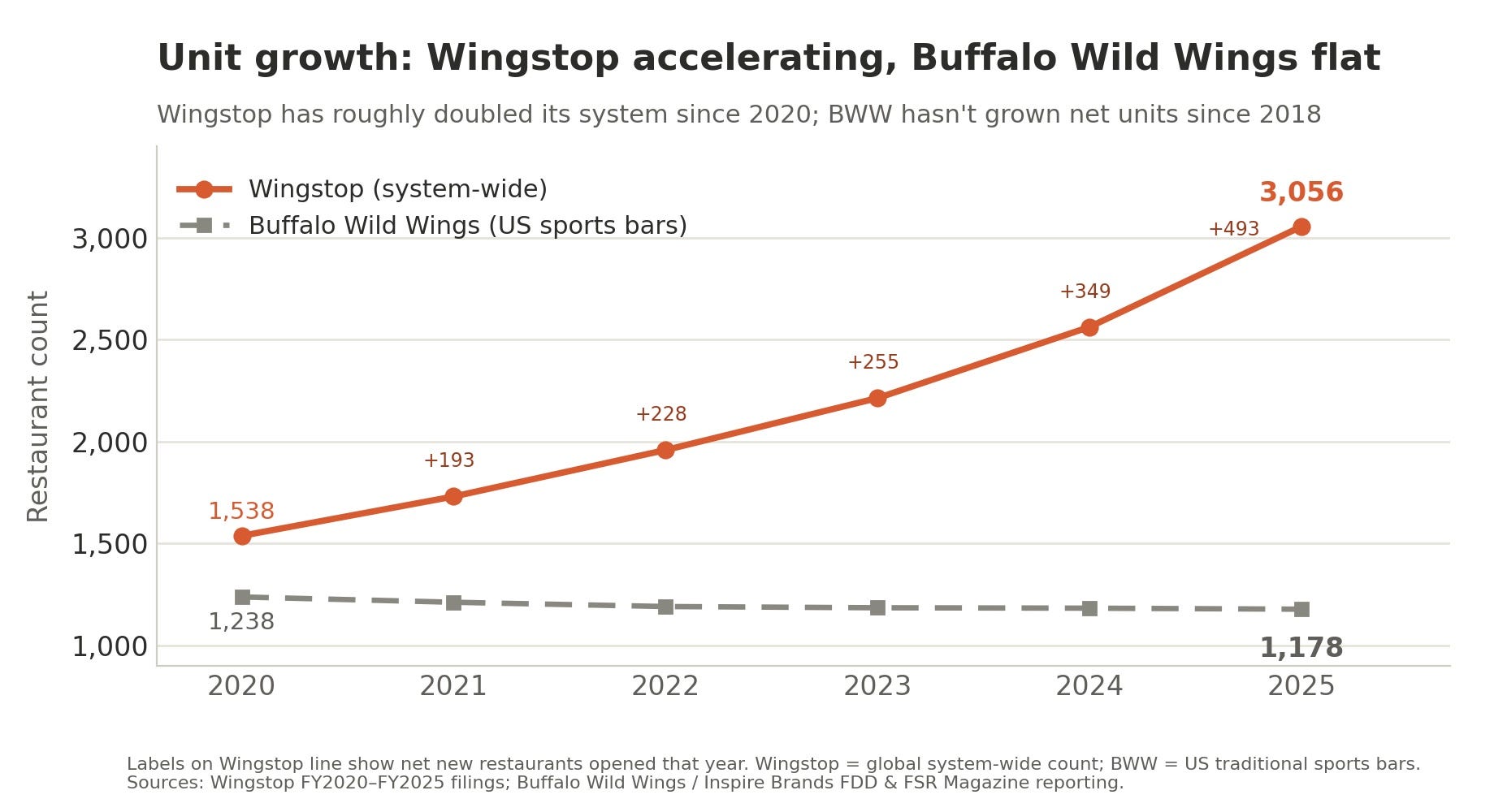

Wingstop’s scale edge in the US is structural and widening. It ended Q1 2026 with 2,653 US restaurants and a pipeline of 2,200+ committed units, so the system keeps compounding no matter what any single quarter’s comps (same store sales growth) do.

Its closest legacy rival, Buffalo Wild Wings, plays a completely different game. BWW runs ~1,180 US sports bars at ~$3.6M AUVs (and a much larger restaurant area, on average, than Wingstop), and the chain hasn’t grown its unit count since 2018. Wingstop added 493 net-new restaurants in 2025 alone. BWW franchisees also spend much more on store setup ($2.5M to $5M).

Popeyes put wings on its menu in 2023, but it's still fundamentally a fried chicken and sandwich chain. And the long tail of regional wing shops has been consolidating for a decade, with Wingstop the main beneficiary.

The bottom line: at its scale, Wingstop doesn't really have competition. It has the most stores, offers the highest returns to its brand partners (likely in my estimates), and is the only growth engine still running, while everyone else is shrinking, defending their footprint, or is too small to matter.

Outside the US, international expansion offers great upside. Since the wing occasion barely exists abroad, Wingstop is building a brand new category instead of fighting established rivals. Beyond mature markets like the UK and Mexico, the brand is expanding its digital model into Canada, South Korea, and Saudi Arabia. These countries will drive near-term growth, but India is the real game changer. With a commitment to over 1,000 stores, India could be a key driver of long-term growth.

The Moat

Wingstop’s durability rests on four reinforcing advantages. Together, they explain why brand partners continue to invest in new Wingstop stores even as consumers are in distress.

Share this with a friend

The franchise royalty model: with high returns on capital for brand partners

95% of 2025 new restaurant openings came from existing brand partners (management commentary), a self-reinforcing loop that strengthens with system tenure. The operators who best understand the unit economics are the ones signing up to build more. Because Wingstop’s model enables high returns for brand partners, they keep investing in the brand and opening more stores. This is a virtuous flywheel for Wingstop, enabling it to scale rapidly.

Flavor IP and a lock on the next generation

Lemon Pepper, Atomic, Mango Habanero, and Hot Honey are flavors that are culturally embedded among younger consumers, backed by 30 years of investment. This is not a vague claim. Millennials and Gen Z make up a large part of Wingstop’s customer base, with 25 to 34 year olds the single largest cohort. The brand earned that position through exactly what those consumers index on - bold customizable flavor, shareable formats, a digital first ordering experience, and ownership of the game day and late-night occasions. The Q1 2026 Hot Honey Trio sold out two of three variants within two weeks. Owning the next generation of restaurant spending is a durable advantage, though a softer one than the franchise structure. Brand affinity erodes if innovation slows.

Structural cost advantage due to small restaurants and sourcing materials at scale

A third moat is structural cost, starting with the restaurant itself. A Wingstop is 1,400 to 1,800 square feet with no drive-thru and barely any dining room. Roughly 90% of sales are off-premise, and more than 70% are digital. This reduces setup costs. The Smart Kitchen concept has recently been implemented, reducing ticket times from about 20 minutes to 10. A large-format competitor with a full kitchen, dining room, waitstaff, and drive-thru cannot get its cost structure down to Wingstop’s level.

Scale shows up in sourcing, too. There is no fixed price market for fresh bone-in chicken wings. Starting in 2024, Wingstop moved most of its system’s wing purchases off the spot market into contracted pricing, giving brand partners cost visibility no independent can match. When wings spike, Wingstop’s franchisees hold their margins while the independent down the street gets squeezed. Smaller formats face similar issues. They can’t get as good a deal as Wingstop.

The data and advertising flywheel

The fourth moat is the one that compounds with scale. Wingstop has a customer database of more than 60 million users, built on a digital mix above 70% that most peers cannot approach, and a national advertising fund that collects 5.5% of sales from more than 3,100 restaurants. A 5,000-store system funds the same Super Bowl spot with far more dollars than a 3,000-store system does, and the first-party data beneath it gets richer with every digital order. As Club Wingstop rolls out nationally (membership plan), Wingstop will monetize its data.

Short-term headwinds vs. long-term opportunity

Short-term Headwinds: Wingstop’s core customer makes the brand more sensitive to macro than its peers. The CFO has said lower-income customers account for roughly 25% of transactions, and gas prices, the labor market, and inflation all hit that customer disproportionately. Two things partly offset this, though. First, even under pressure, these customers are trading up into larger bundles rather than trading down (ordering larger sizes), so ticket has held steady even as people have cut back on ordering extras, etc. Second, management is deliberately focusing new customer acquisition on the $50K-$100K household income cohort, thereby reducing reliance on lower-income cohorts.