Deep Dive: XPEL

High quality market leader in an oligopoly industry

XPEL’s most famous product (and most significant revenue generator) is its Paint Protection Film (PPF). This is a see-through film applied to hoods, bumpers, fenders, and often the full body of cars to protect from chips from road debris, gravel, and stones. The film keeps paint looking new, which protects resale value.

Kelley Blue Book and Edmunds, the two pricing guides American dealers and shoppers rely on to value a used car, both grade a vehicle's condition partly on its paint, and chips, scratches, or a dull finish drop it a grade and knock down the price. Pristine paint is rarer than people think. Only about 5% of used cars clear Edmunds' top ‘Outstanding’ grade, and everything below it gets marked down for the cost of reconditioning the paint, which dealers subtract from their offer. Clear PPF keeps that factory finish intact, and because it is invisible it sidesteps the resale penalty a visible wrap can carry. XPEL is the name buyers and installers ask for, the most recognized premium film in a category it has out-grown for a decade.

XPEL started in San Antonio in 1997 to write software, not to make film. That software, called DAP (Design Access Platform), is a digital library of cutting templates. An installer enters a car's make, model, and year, and DAP drives a machine that cuts the film to the exact shape of each panel on a bench, before any of it touches the car. That removes the slow and risky part of a wrap, hand-trimming film on the vehicle, where one slipped blade can scratch the paint. DAP arrived in the mid-2000s, years before XPEL made film at scale. So this is a software business that grew into film, not a film company that bolted on software, and that is why it keeps taking share from rivals a hundred times its size. It helps that its customers, thousands of small dealers and installers, have no real leverage over price.

Welcome to Rebound Capital. We study beaten-down stocks and businesses that have made successful comebacks. Subscribe for free to join our growing community of 22,500+ subscribers and make sure you don’t miss our next briefing.

The stock peaked above $100 in 2021 and now trades around $45, roughly 56% below that high. The de-rating was due to 1 soft year in 2024, a short report in 2023, and a US auto market that's been visibly weak into 2026. Based on our research, we believe the market is overlooking multiple catalysts over the next 2 years that could transform XPEL into a higher-quality business.

How XPEL makes money

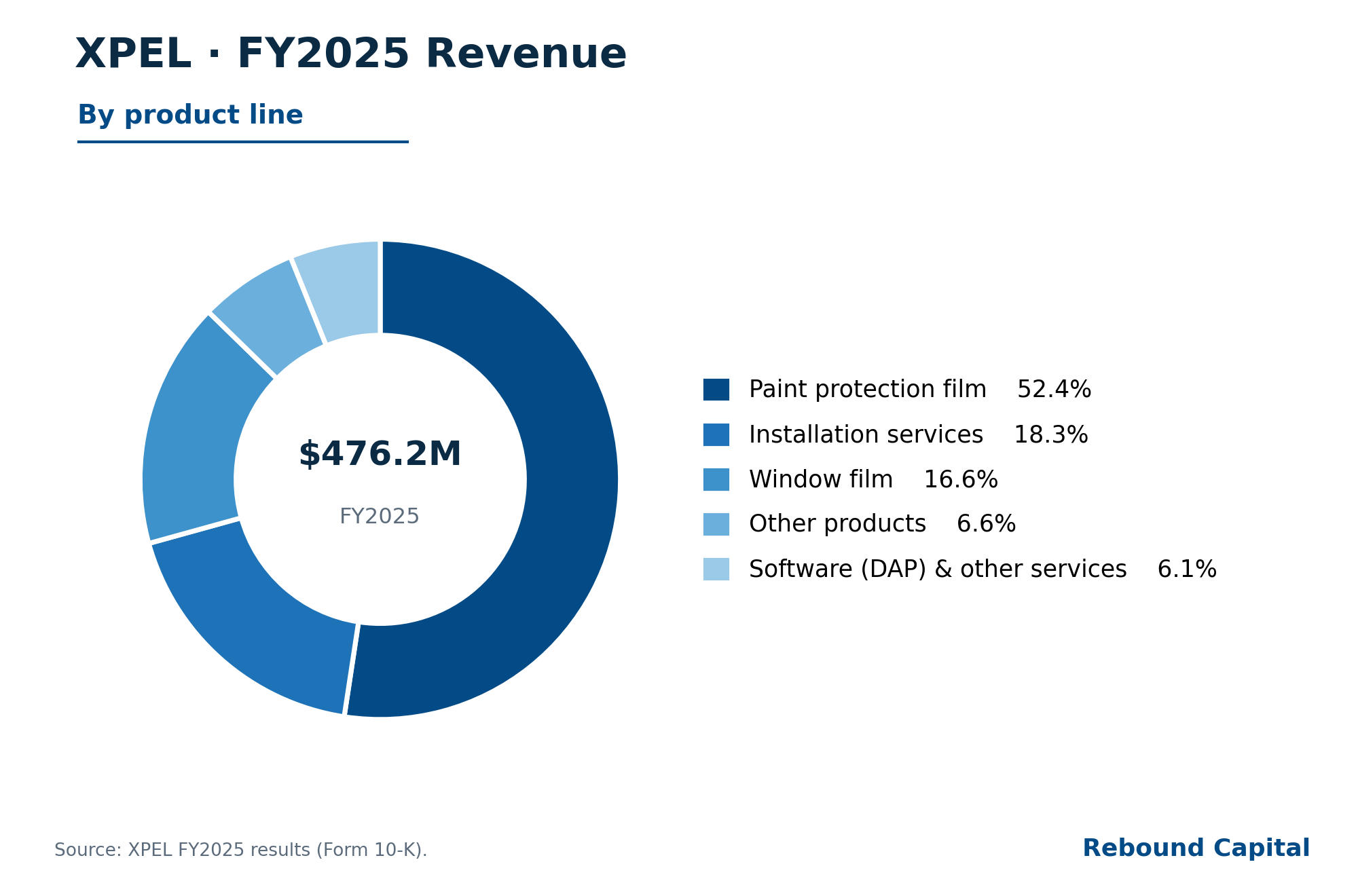

XPEL earns revenue from 4 major product lines:

Paint protection film (PPF) is the flagship, about half of revenue. It’s a urethane film cut to a car's exact panels to stop chips, scratches, and staining. XPEL sells the most expensive film in the category. Despite higher prices, they have been gaining market share (XPEL’s growth rate has been higher than the PPF market’s mid to high single digit growth).

Window film accounts for ~16% of revenue, including automotive tint under its own brands (PRIME).

Installation services are about 18% of revenue and growing. But installing is not how XPEL mainly makes money. Most of its film goes out wholesale. XPEL supplies the film, the DAP software, and the training to thousands of independent installers and dealerships. They do the work and keep the labor fee. XPEL keeps the product margin. The installation line is where XPEL does the job itself, through 34 company-owned centers and the labor it runs inside dealerships and at OEM plants. On those cars it takes the labor margin too, not just the film, and it learns first-hand what buyers choose and what they come back for. We read it as a deliberate step up the value chain in select markets, not XPEL's main route to the customer.

DAP software is under 5% of revenue, but it earns far higher margins than the rest of the business - closer to pure software than to the low-40s gross margin XPEL earns overall. It is also the deepest part of the moat. This software provides the correct PPF film for any car model that requires protection. There are more than 90,000 configurations - due to the number of different car models, the different versions of the same car over the years, and so on.

Cut the wrong pattern and you have to scrap the film. That’s a few hundred to a couple thousand dollars wasted. Botch the install and the whole job gets stripped and redone, film and labor both, which on a premium wrap is $5,000 or more. And if a bad install or its removal lifts the paint, the owner is repainting panels at $500 to $3,000 each. That is the cost of getting it wrong, and why the software is important.

So the software that cuts the film (see video below) is a deep moat. Competitors have not been able to match the depth of configurations in XPEL’s DAP software.

The moat: why XPEL beats 3M and Eastman Chemical

XPEL goes up against 3M and Eastman, two industrial giants with R&D budgets that it can’t match. And yet it is gaining share driven by its DAP software, brand, and vertical integration.

DAP Software

When an installer wraps a car, the hard part isn't sticking film to metal. It's cutting hundreds of vehicle-specific shapes without scratching the paint, where one slip means a repaint that costs thousands. DAP lets an installer enter the make, model, and year and pull up a ready-made pattern. This cuts installation time by an estimated 25%-70%.

XPEL holds about 60% of the pattern-software market, a larger share than it holds in the film itself, and the software lead tends to pull film share up behind it.

The library is only the start. Once a shop runs DAP, it accumulates customer history, work orders, plotter calibrations, and warranty submissions within the system. Many shops carry several film brands but run DAP for all of them.

Brand

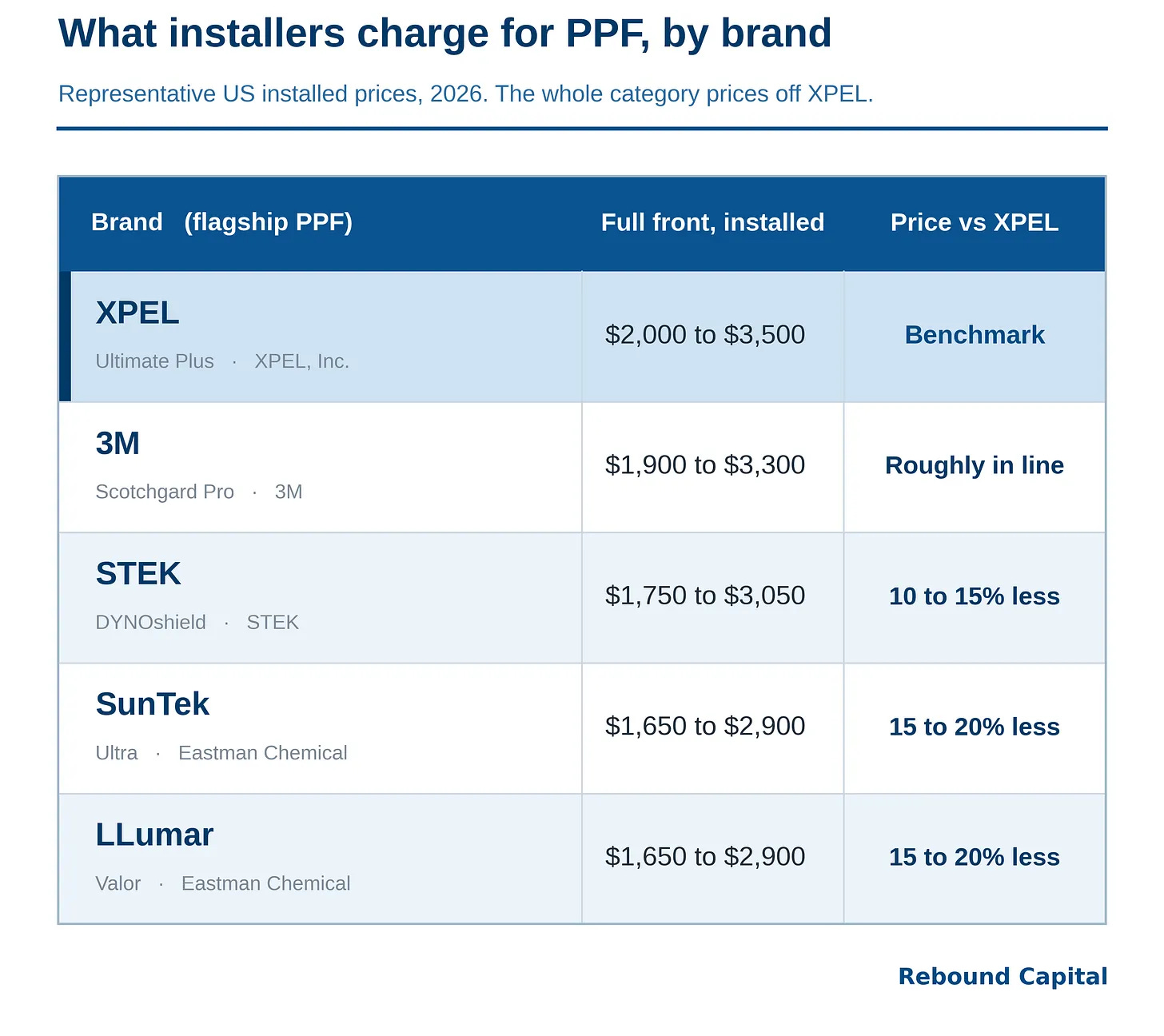

XPEL can charge higher prices for its products. This is its brand power in action. Installers quote SunTek and LLumar as a set percentage below XPEL. Dealers and installers charge more than 3M or Eastman product, protecting XPEL's pricing and its partners' margins. Like for like, XPEL runs about 15 to 20% above Eastman value films and is on par with or above 3M, the other premium name.

Vertical Integration

Over the past 6 years, XPEL has acquired distributors in Canada, France, Australia, and India, took a 76% stake in its China distributor in September 2025, and built its own installation network. In November 2025, XPEL said it would bring film manufacturing in-house with a $75 to $150 million investment. In May 2026, XPEL announced plans to spend ~$110 million on a 435,000-square-foot, four-building site in San Antonio that will become its North American manufacturing hub, and the purchase of a film manufacturing facility in China. Once both are running, XPEL will own software, manufacturing, distribution, installation, and a slice of retail. No other PPF brand is vertically integrated to this extent. This helps XPEL deliver higher profit margins.

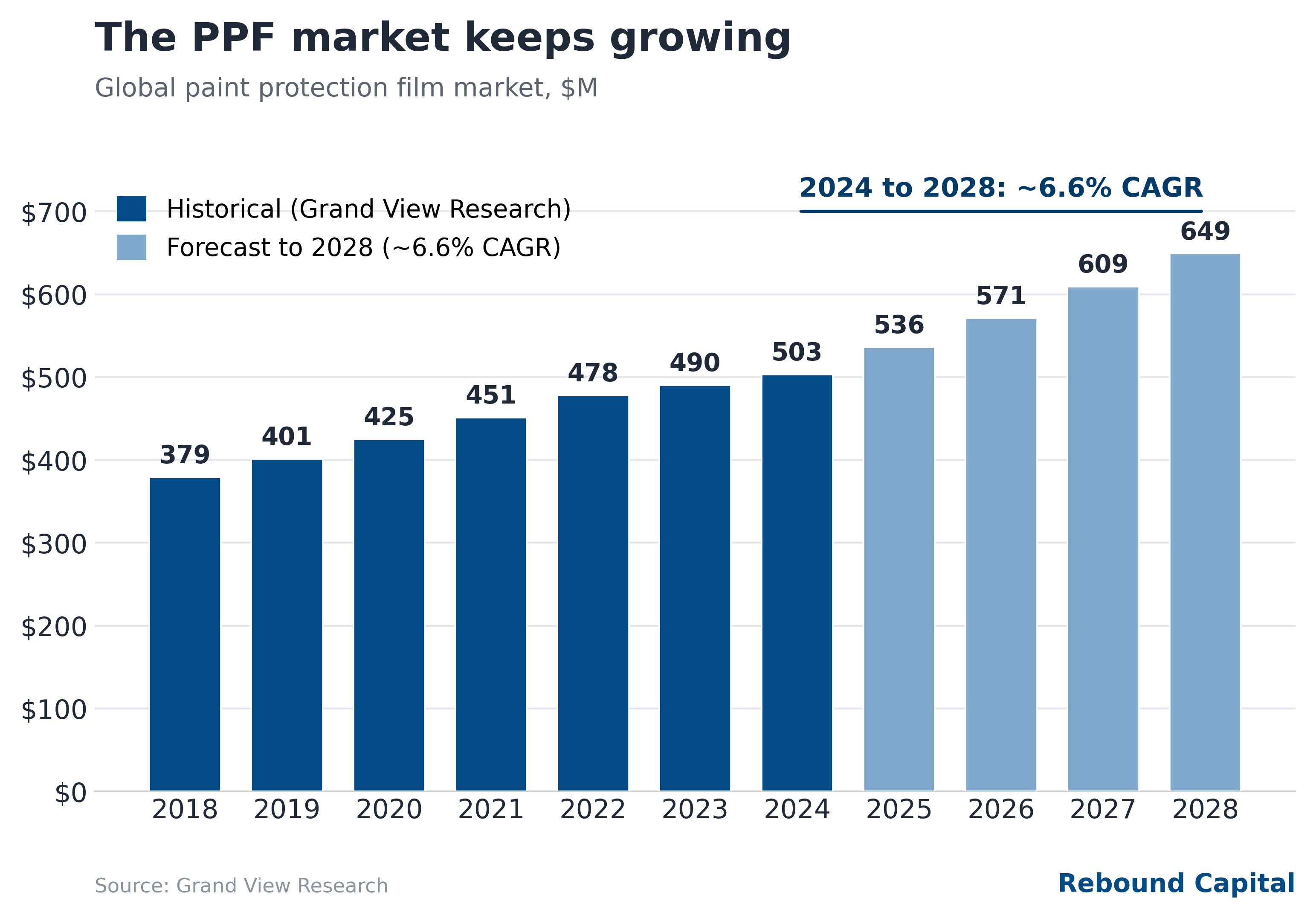

PPF market’s secular growth

XPEL’s share gains would matter less if the pond were drying up. It isn’t. Independent estimates put the global PPF market near $500 million in 2024 and on track for roughly $650 million by 2028, a mid-to-high single-digit annual pace. The US sits around $105 million and grows about 6% a year. International runs faster. Europe is the largest single region today, and management likens it to where the US stood five years ago. Asia Pacific grows quickest, led by China and India.

One caveat we won’t paper over. These third-party figures scatter badly, from under $400 million to north of $1.3 billion, depending on whether a firm counts raw film, installed retail, or something in between. The low end is hard to square with XPEL’s own PPF revenue of roughly $240 million, which tells us the real installed market is a good deal larger than the headline numbers imply. So we anchor on the one thing every source agrees on: the direction. The category compounds in the mid-to-high single digits, pushed by longer vehicle ownership (the average US car is now past 12 years old), rising resale-value awareness, EV adoption, and film that heals its own scratches.

For XPEL the takeaway is simple. It has out-grown this market for a decade, taking share on top of a base that is itself expanding. That is two tailwinds, not one, and it is why we don’t read XPEL as a slice of a shrinking niche.

What went wrong

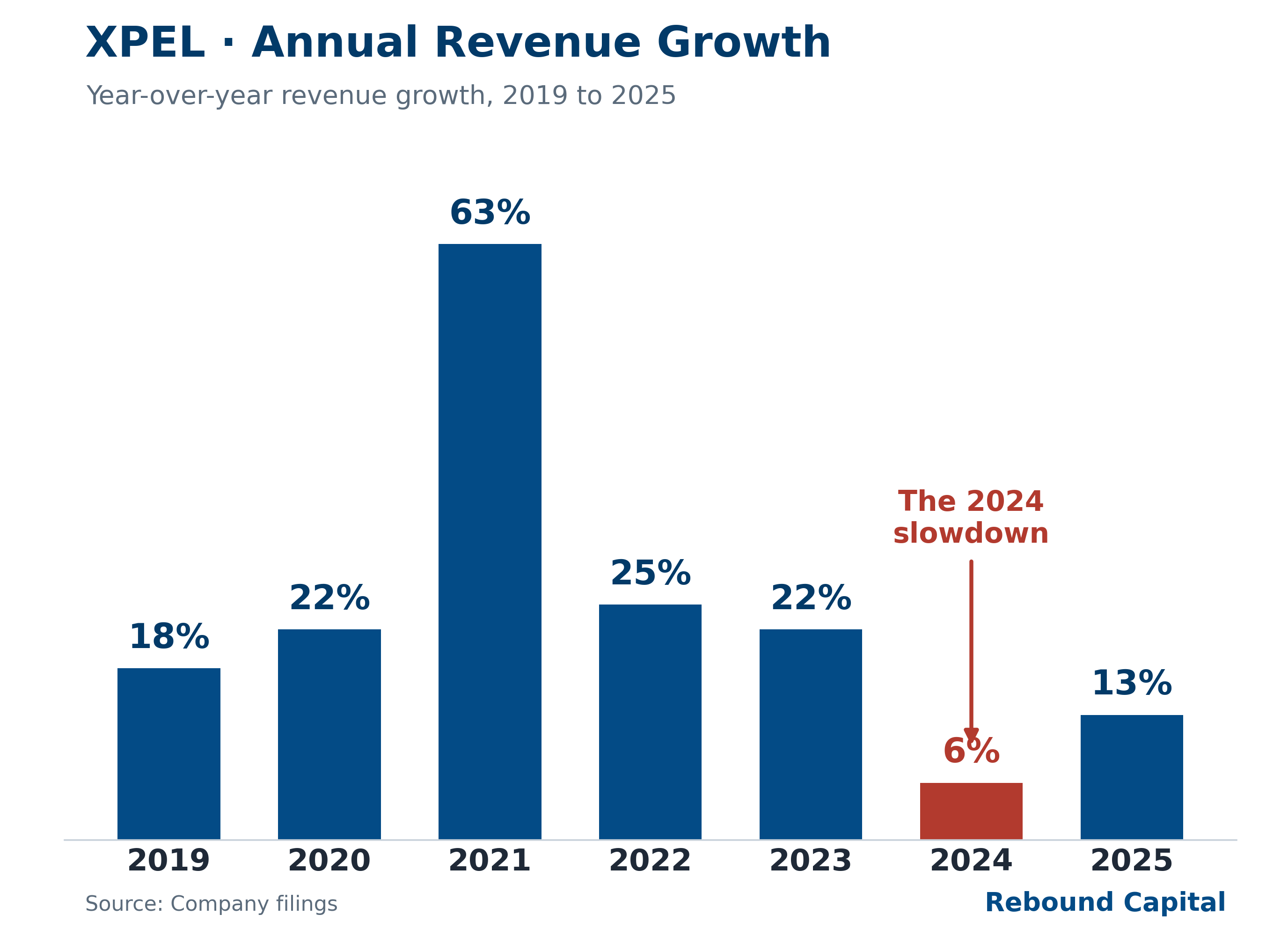

The 2024 air pocket

After four years of 22 to 63% growth, revenue slowed to about 6% in 2024. The slowdown was driven by a Chinese distributor de-stocking, post-COVID luxury digestion, and a transition in the Tesla and Rivian channel. By Q1 2026, growth was back to 13%.

The 2023 short report and Tesla scare

Two negative catalysts in 2023 pressured the stock. One was a short report by Culper Research & the second was fears that Tesla would do its own PPF and that Tesla is a large part of XPEL’s revenue. The shorts argued that Tesla accounted for 25%-35% of sales, that a PPG and Entrotech joint venture would launch an OEM paint product that would kill PPF, and that OEMs would insource and commoditize the category.

None of the elements of the short thesis worked out. Management put Tesla at about 5% of sales, a fraction of what the report implied. The PPG paint product is real, but it still has not displaced aftermarket film, and XPEL grew revenue 13% in 2025 anyway. OEM insourcing never showed up either. Wrapping a car is fiddly work, fit by hand panel by panel, and it does not drop cleanly onto an assembly line. If anything, XPEL has done the opposite of getting squeezed out. It now runs the OEM channel as a tailwind, with Tesla sending buyers straight to XPEL and Rivian offering the film factory-installed.

The macro

The US new-vehicle market has been soft into 2026, with year-over-year declines. Because the market still treats XPEL as an auto cyclical, a weak vehicle market weakens sentiment.

Re-rating catalysts over the next two years

The key business drivers are all heading the right way.