Notes on Nvidia ($NVDA)

Sizing up NVDA's TAM and Valuation

NVIDIA heralded the AI age. It holds a near monopoly on general-purpose GPUs used for AI training and inference. The nearest competitor is Broadcom, which makes custom chips for large customers, but Broadcom’s AI data center revenue is ~$25B vs Nvidia’s ~$194B in the last twelve months. AMD, the closest general-purpose GPU competitor, reported less than $10B in revenue over the last 12 months.

Why is it down?

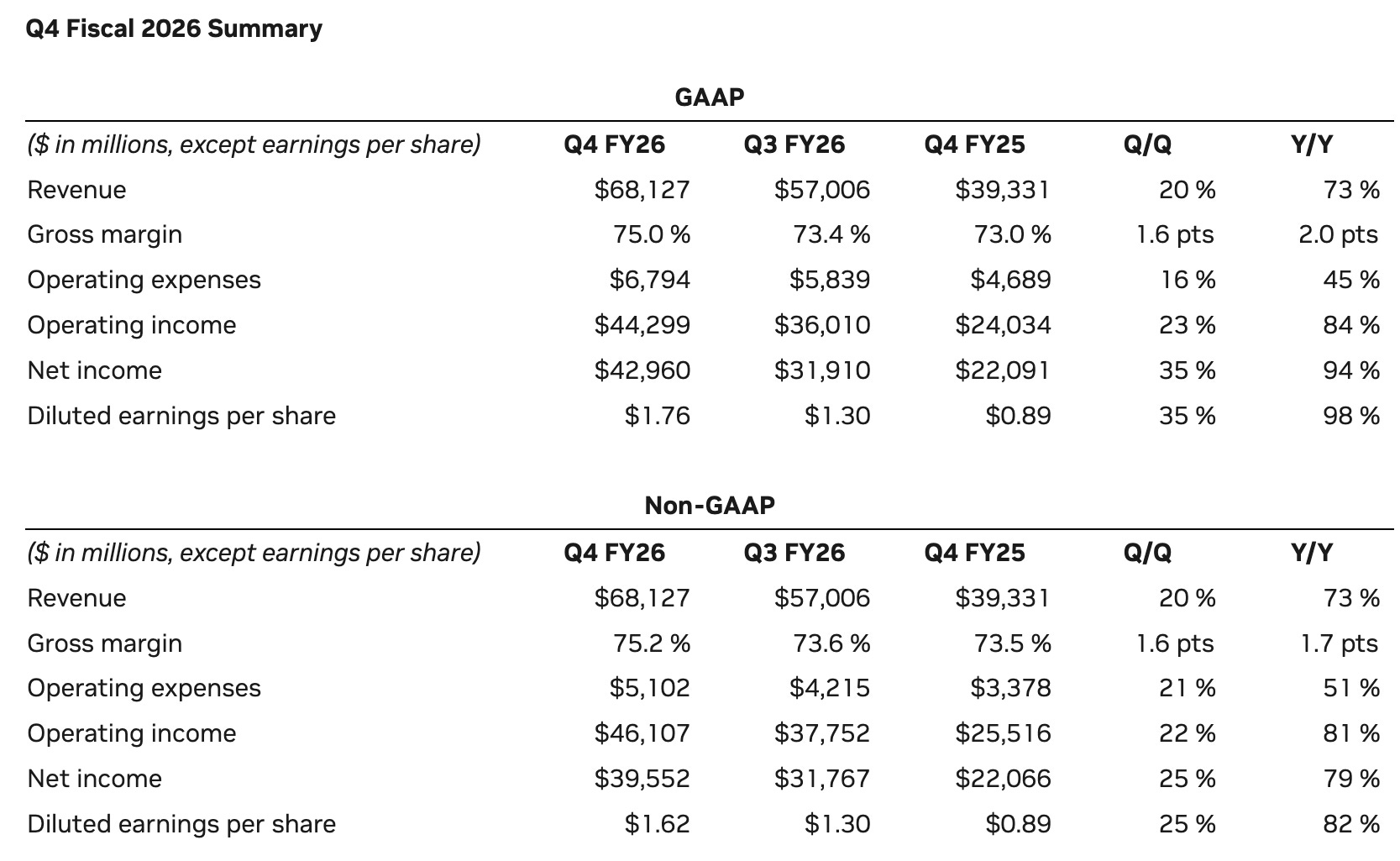

As of March 30, 2026, Nvidia is trading near $165, reflecting a roughly 20% correction from its recent all-time high of $212.19. Despite reporting record-breaking fiscal 2026 revenue of ~$216 billion, the stock has entered a ‘risk-off’ phase as investors pivot from chasing momentum to a more defensive stance.

‘Sell the News’ at GTC 2026: Even after CEO Jensen Huang announced a $1 trillion pipeline for the new Blackwell and Vera Rubin architectures (through 2027), the stock failed to rally. Investors have largely ‘priced in’ this growth, leading to a classic ‘sell the news’ reaction where even strong guidance wasn’t enough to sustain the rally.

Geopolitical and Macro Volatility: Ongoing conflict in the Middle East and renewed U.S.-Iran tensions have rattled global markets. Furthermore, the 25% tariff on AI chips and proposed per-customer caps on sales to China have limited Nvidia’s ability to fully capture revenue from the world’s second-largest AI market.

Customer Concentration: Recent filings revealed that just four customers (likely Big Tech hyperscalers) account for over 60% of Nvidia’s revenue. As Meta, Alphabet, and Amazon accelerate the rollout of their own custom silicon (such as TPUs and Trainium), the market is pricing in a potential peak in GPU demand.

Antitrust Pressure: In mid-March, a preliminary EU antitrust probe into GPU bundling and a U.S. Senate inquiry into the Groq deal created regulatory overhang.

NVIDIA’s current business performance is stellar. The market is questioning whether the company can sustain strong growth in the coming years. The ~20% drawdown occurred after Nvidia reported 73% YoY revenue growth and guided to 81% YoY growth in the coming quarter!

From our perspective, given the myriad news cycles (AI ROI doubts, trade war, actual war), the market is overlooking the fact that the world is highly compute-constrained.

Below, we attach the pricing for compute rental. The trend is clear. Even older generations of GPUs, like the A100s, are seeing rental prices rise.

This pricing increase, coupled with strong commentary from the AI industry, gives us confidence that this infrastructure cycle is still early and that demand for Nvidia’s chips will continue to grow in the coming years (as AI use cases continue to explode).

The price of compute has gone up materially since the start of 2026, following the latest viral Copilot Cowork and other enterprise use cases, such as coding and agentic workflows. The TAM for AI is not just about increasing workers’ efficiency but also about adding agentic knowledge workers (essentially, the TAM is much larger for agents than it was for training models). And Nvidia’s GPUs turn electricity into autonomously working agents! The market is underestimating the demand for compute once agentic AI takes off. 2026 is the year in which this massive change plays out. The market is too distracted by the war to realize this.

Edit: A day after our Nvidia notes were released, SemiAnalysis made the following pricing graphs public. Their data is further proof of our thesis that compute demand is inflecting, and we are in the midst of a compute shortage - which will directly result in higher revenues for Nvidia.