Earnings Review: $AXON, $NVDA, $BIRK, $CRM, $TOI, $RACE

And sector takeaways

We are publishing this without a paywall.

In this earnings review of Axon, Nvidia, Birkenstock, Salesforce, Topicus, and Ferrari, we will also focus on the key takeaways for their respective sectors. We aim to determine whether there have been any major AI-driven changes in these sectors (pricing, customer retention, customer preferences, etc.) and whether these earnings lead us to change our thesis on any portfolio names.

We have recapped our thesis on each stock in our portfolio in the March Portfolio update.

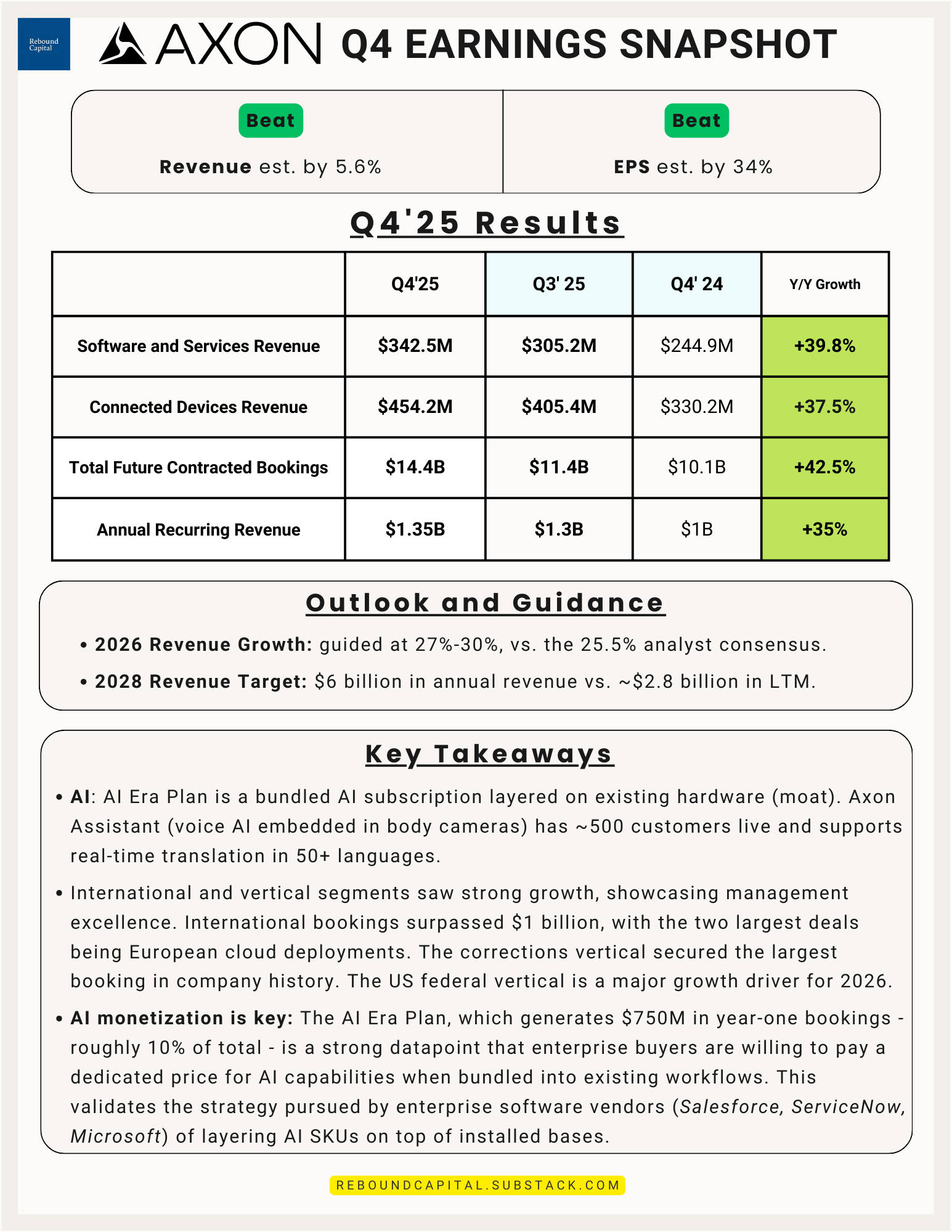

Axon ($AXON)

Takeaways for the Software Sector

Axon’s results carry several meaningful signals for the broader software sector. We notice the following trends:

AI monetization is key: The AI Era Plan, which generates $750M in year-one bookings - roughly 10% of total - is a strong datapoint that enterprise buyers are willing to pay for AI capabilities when bundled into existing workflows. This validates the strategy pursued by enterprise software vendors (Salesforce, ServiceNow, Microsoft) of layering AI SKUs on top of installed bases.

Markers of AI success: For AI to be seen as a positive catalyst, the market will require evidence of either accelerated growth or expanded margins for SaaS businesses. Axon’s strong revenue growth led to its re-rating (Axon is up ~30% since its earnings). Its combined hardware-and-software moat benefits from, and is not disrupted by, Gen AI.

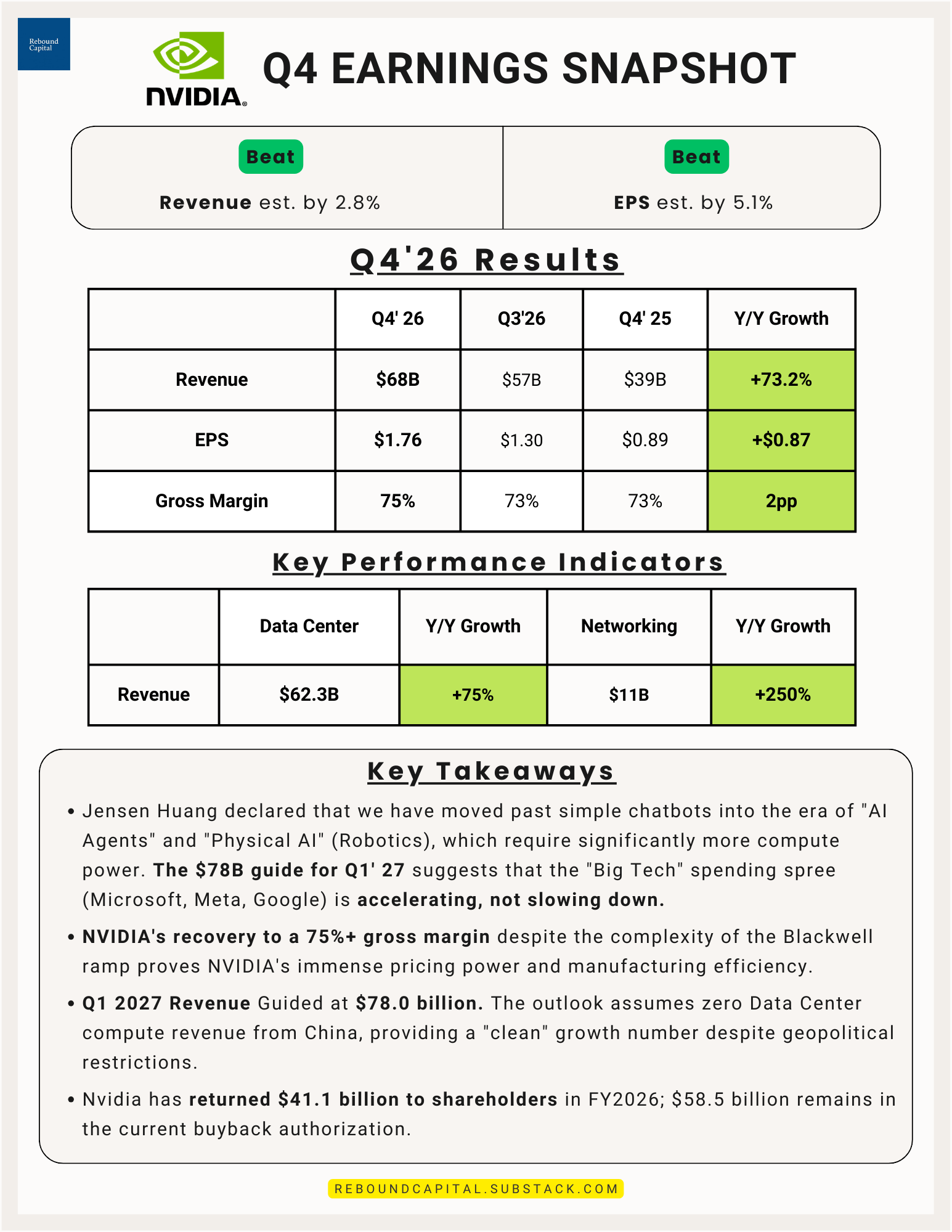

Nvidia ($NVDA)

Takeaways for the AI Trade

The results solidify the fact that the AI trade is alive and well. The market may be jittery about Nvidia's incremental growth, but enterprise AI use cases are just getting started. This will benefit our core holdings of Amazon, Alphabet, and AMD.

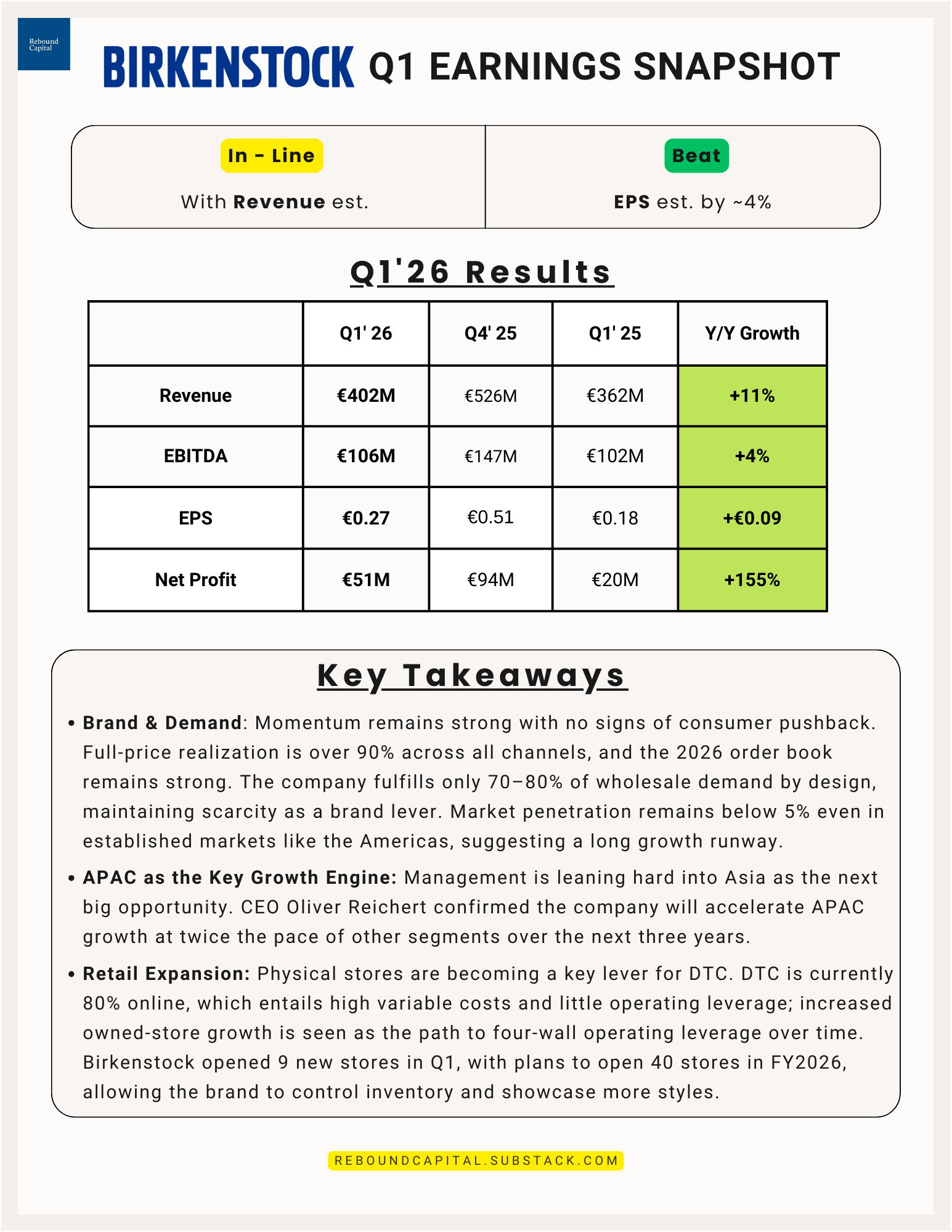

Birkenstock ($BIRK)

Conference Call Highlights

The Birkenstock brand is strong. Growing at a high double-digit rate in a weak consumer environment is commendable. Birkenstock’s deliberate under-fulfillment of wholesale demand (70–80%) keeps brand desirability elevated and supports full-price sell-through above 90%. This validates the playbook used by luxury and premium footwear brands - constrained supply protects pricing power even in softer macro environments.

The second takeaway is that the growth journey in APAC is just getting started. Birkenstock’s 37% revenue growth in APAC on a constant-currency basis (in Q1 2026) is a strong data point that Asian consumers are embracing Birkenstock’s products.

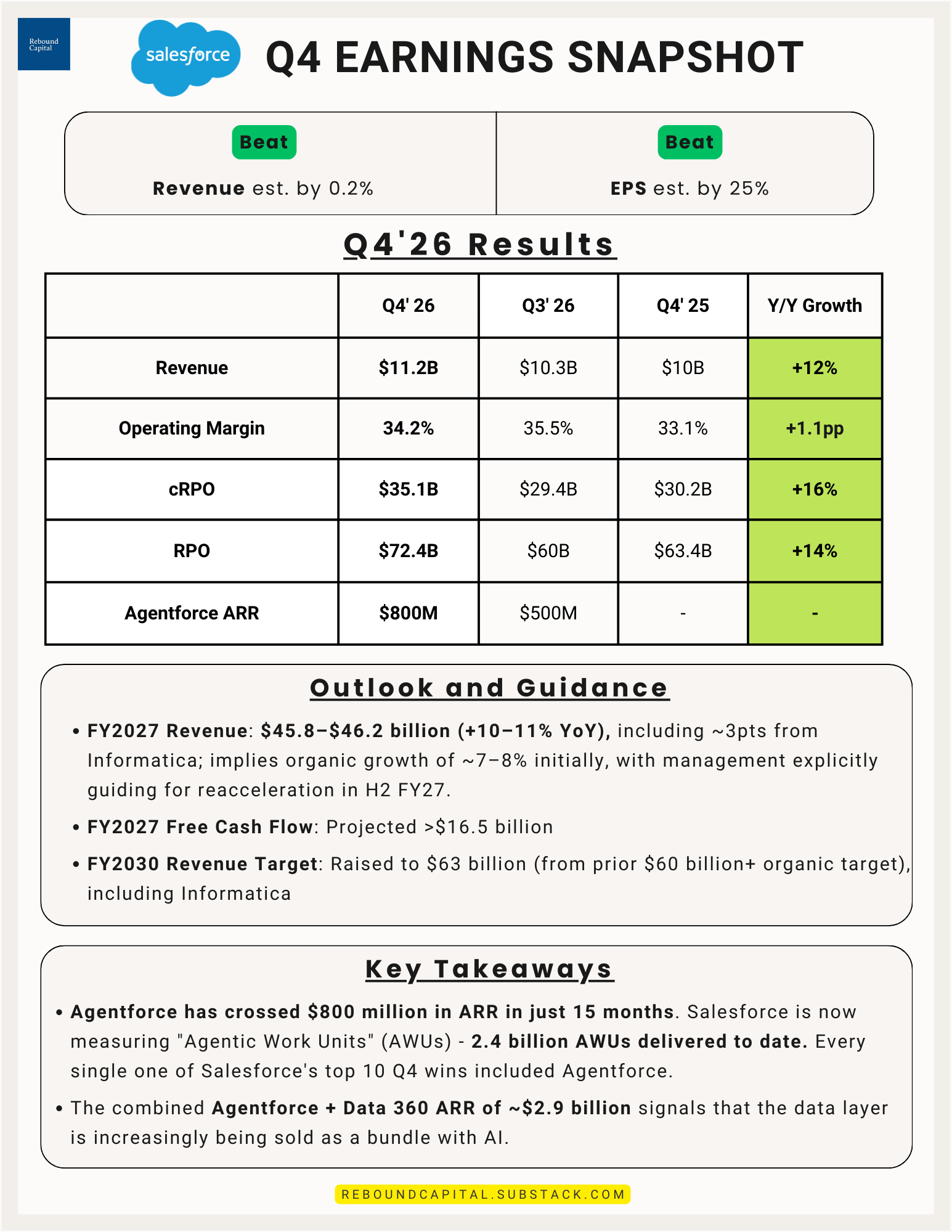

Salesforce ($CRM)

Takeaways for the Software Sector

Agentic AI is the main product being sold. “Agentic Work Units” as a metric is a harbinger of consumption-based pricing across enterprise software. Salesforce began disclosing AWUs, the number of discrete tasks agents completed, as a parallel to tokens in LLM pricing. This signals that the enterprise software industry may shift, over time, from pure seat-based or subscription pricing toward outcome or consumption-based models. Software companies that own infrastructure-level data and workflow layers (Snowflake, ServiceNow, SAP) will be best positioned to participate in this transition. The key metric to watch will be the gross margins on this revenue.

The installed base is the most valuable asset in the AI era. More than 60% of Agentforce and Data 360 bookings came from existing customers. The single most important structural advantage Salesforce has is 150,000+ enterprise customers who already trust its platform with their CRM data. This is the read-across for any SaaS company with a large installed base: the moat is not the AI itself. It is the trusted data and the existing relationships that allow AI to be deployed with minimal friction.

Legacy software is beginning to be displaced, not just supplemented. SaaStr’s CEO mentioned live on the call that agents running on Salesforce are already replacing Marketo, a separately purchased marketing automation platform in their stack. This is an early but significant signal: as agents handle end-to-end workflows, the need for point-solution software sitting between systems may decline.

Consistent with what we flagged in the Axon and Snowflake notes, the market wants to see revenue growth reacceleration, not just momentum in ARR or bookings. Salesforce stock sold off after the company’s organic revenue growth guidance for FY27 disappointed.

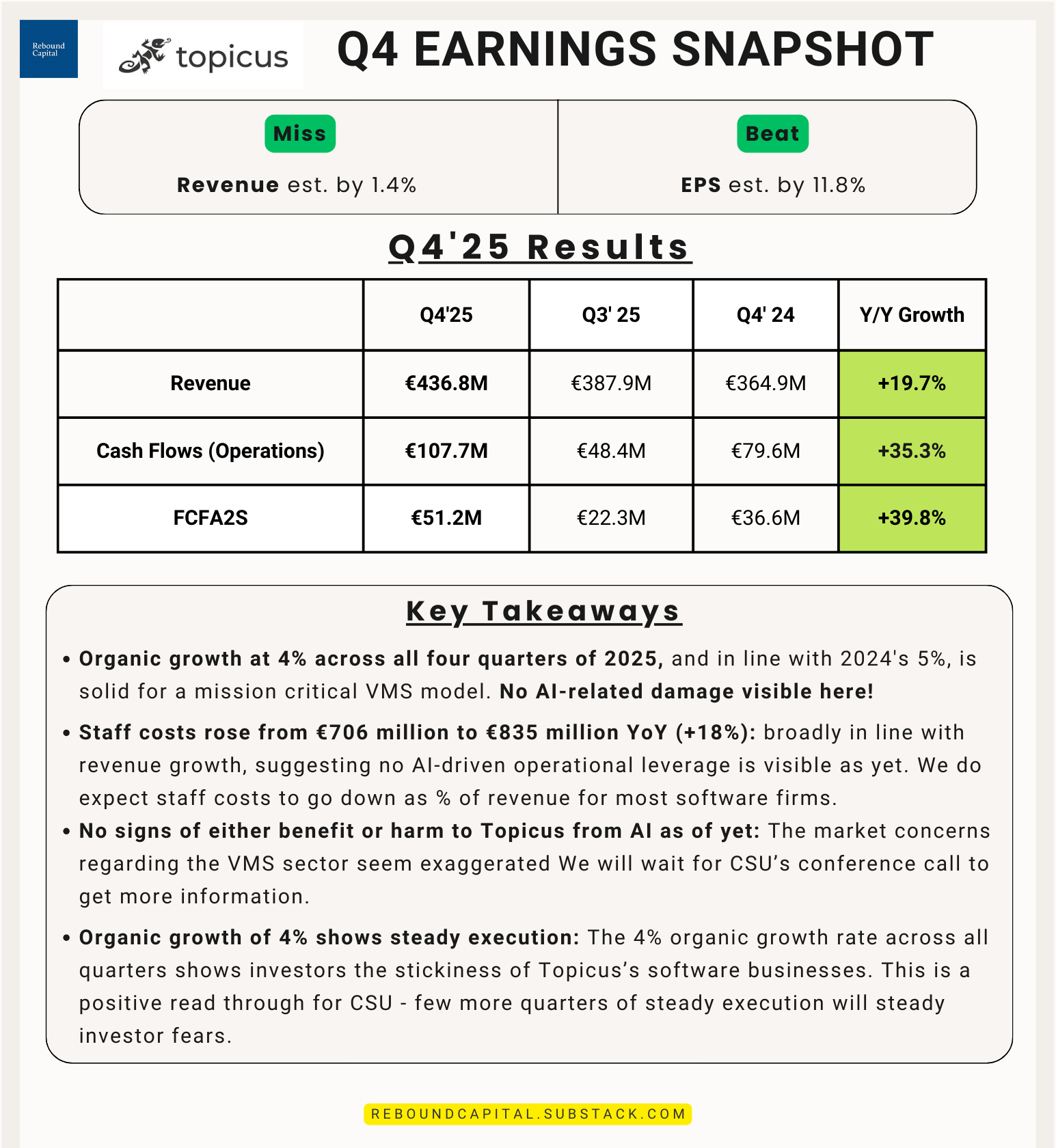

Topicus ($TOI)

Takeaways for Vertical Market Software & $CSU

Topicus is a large subsidiary of Constellation Software. Its results offer us a sneak peek at how $CSU itself is expected to report next week.

Topicus’s results carry several meaningful signals for the broader software sector. There are no signs of either benefit or harm to Topicus from AI as of yet. Market concerns about the VMS sector seem exaggerated. Organic growth of 4% shows steady execution and that customers are still expanding with Topicus. This is a positive read through for CSU - a few more quarters of steady execution will steady investor fears. In fact, Constellation Software is now up ~20% in the past month.

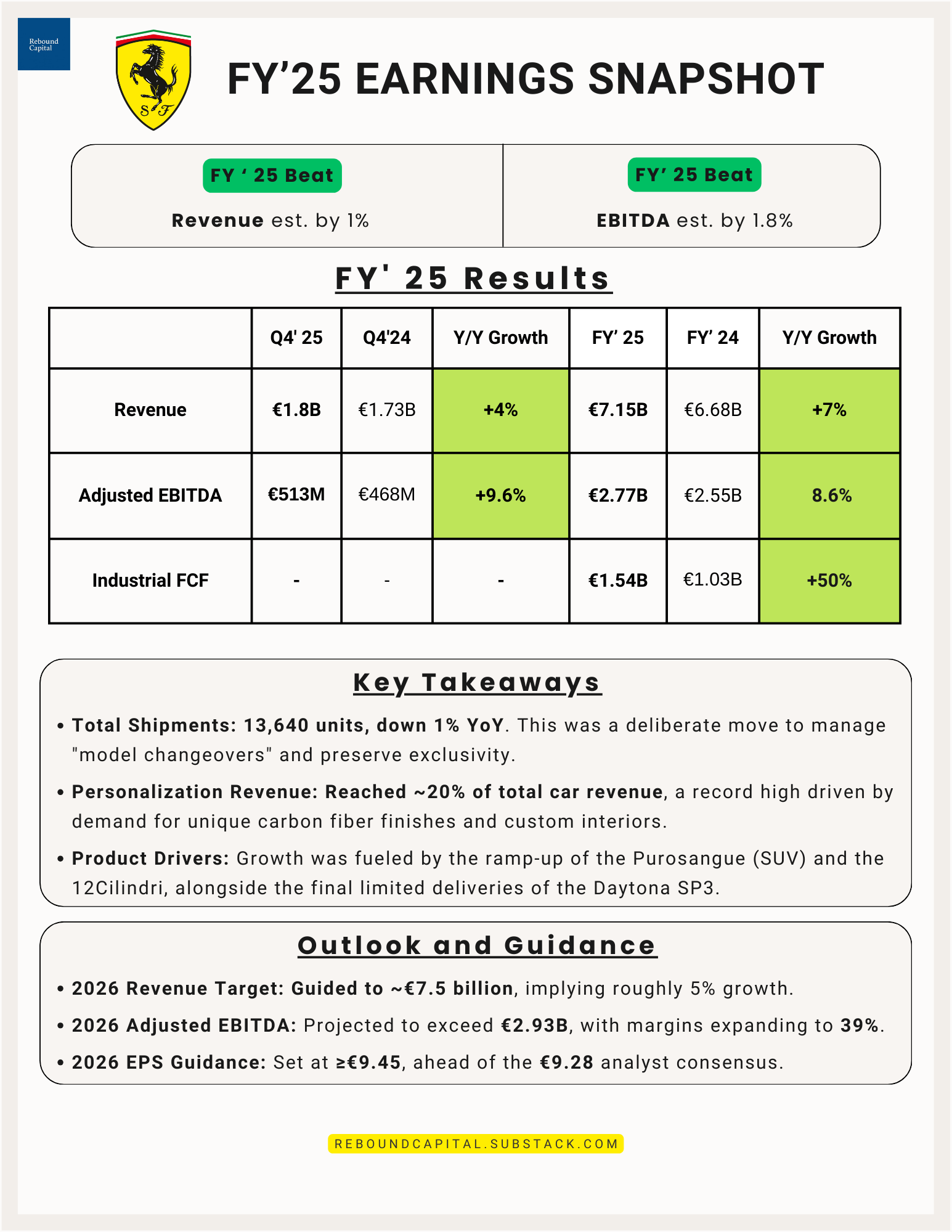

Ferrari ($RACE)

Conference Call Highlights

Ferrari officially teased its first fully electric vehicle (EV), named Ferrari Luce, with a world premiere scheduled for May 25, 2026, in Rome. CEO Benedetto Vigna noted that Ferrari will not use “forced” EV sales to meet quotas, instead relying on the high technological content of the Luce to command premium pricing.

Sponsorship and brand revenue jumped 22%, aided by a better Formula 1 ranking and the success of new “lifestyle” flagship stores in London and New York.

The board announced a massive new €3.5 billion share buyback program to be executed through 2030, signaling extreme confidence in future cash generation.

Takeaways for the Luxury Sector

Ferrari’s results suggest the ultra-luxury consumer remains entirely decoupled from the high-interest-rate environment affecting mass-market automakers like Ford or VW. This is a net positive for our holding in LVMH (as its biggest segment caters to the ultra-wealthy), as it shows that, despite a tough environment, wealthy consumers are still spending, given they derive prestige from buying luxury goods. LVMH will need to navigate the current environment deftly and then resume its growth journey in the coming years.

By targeting a 39% EBITDA margin as it launches its first EV, Ferrari is signaling to the market that electrification need not be margin-dilutive if the brand equity is strong enough.

That’s it for now. If you are here, please “♡ Like” this piece. It helps us massively!

Rebound Capital’s work is provided for informational purposes only and should not be construed as legal, business, investment, or tax advice. You should always do your own research

I thought Topicus has been spun off from Constellation SW...does Constellation still have an equity position in it?