Notes on SaaS

Will AI disrupt SaaS

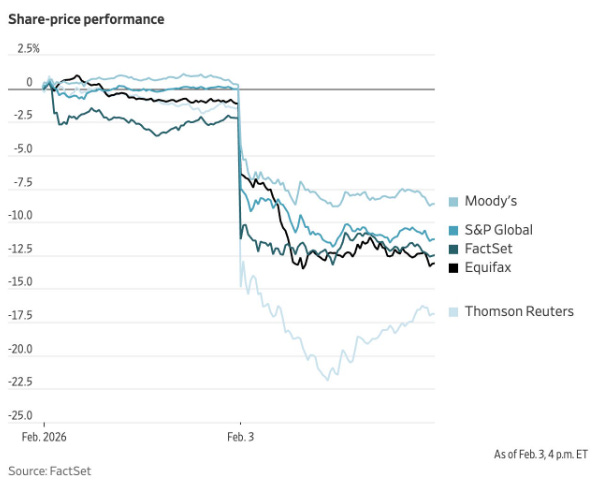

Yesterday was one of the worst one-day drops for software companies with high-quality names, including ServiceNow down 7%, Adobe down 7%, and one of our picks, Constellation, down 6%. Everything started with Anthropic releasing Cowork assistant for legal users, which can now automate high-stakes tasks such as contract reviews and compliance workflows.

Investors are now left wondering whether traditional Software-as-a-Service (SaaS) can compete with AI agents that can perform most work autonomously and will likely charge per task rather than the fixed per-seat pricing of SaaS companies.

With ~13% of our Rebound Portfolio in software names, let’s dig a bit deeper into what’s driving the current meltdown and if we should be worried!

Welcome to Rebound Capital. If you are new here, we conduct in-depth research on beaten-down stocks and study companies that have made successful comebacks. Subscribe for free and join 18,200 other investors to make sure you don’t miss our next briefing.

We present the drivers of the software meltdown and assess the merits of each.

Agentic AI led disruption

When Generative AI first emerged, SaaS firms’ playbook was to use foundation models from hyperscalers or OpenAI/Anthropic, then train and fine-tune them for specific use cases. The market now believes that, rather than augmenting software, Agentic AI may directly perform tasks for users (bypassing the need for traditional software). Since SaaS firms are not developing their own foundation models, they will be disintermediated by firms like Anthropic.

Our Take

The market is discounting the effort required to implement software for customers. It’s not just downloading an agent and running it. Hence, it seems simplistic to assume that the same companies that build foundation models will also sell, maintain, and tune those agents for enterprises.

However, SaaS will need to adapt. Many horizontal SaaS companies have massively increased their product prices over the last decade (especially as they shifted from the license to the subscription model). They will need to reprice their products based on outcomes and shift away from per-seat pricing. Many large software firms have strong customer relationships and real-world experience that can be leveraged. However, they will need to sell outcomes rather than features. They need to sell agents and not software.

For vertical market software (VMS) firms, we expect that AI will enable them to deliver more value to their customers. Many VMS firms develop software for niche industries, and their customers allocate a small share of their total budget to mission-critical software. We expect this segment to be less affected by AI, as VMS software has always been designed to deliver clear-cut outcomes and its moat is based on industry expertise. VMS firms will also need to start delivering agents to their customers, where required.

Expensive Valuations

Software has been one of the highest-valued sectors since 2018. As SaaS transitioned from a license to a subscription model, the market rerated them higher.

Given their rapid growth (>50% YoY in many cases), the markets valued them on a non-GAAP basis to allow for the high expenses required for such growth. For example, the markets overlooked the substantial stock-based compensation (SBC) these companies granted to employees and valued SaaS on free cash flow multiples (which do not account for SBC). This adjustment overstated SaaS profits, but investors were comfortable with it. The logic was that SBC would eventually reduce as these companies scale.

Another way the market valued SaaS was on a revenue multiple! In traditional discounted cash flow analysis, companies are valued based on their free cash flow. Investors were paying up to participate in the growth story.

The 2 factors above caused software firms to be massively overvalued on a GAAP basis (i.e., earnings excluding expense adjustments). Many software firms are falling because they were too expensive to begin with.

Our Take

Software will now be valued based on GAAP earnings and free cash flow available to shareholders. This means that stock-based compensation will be counted as an expense. The market will reward software companies that minimize costs, improve productivity, and transition to clean GAAP-based reporting.

AI-native companies

Another fear is that companies born in the AI era will be able to develop software rapidly and then undercut established software firms on price.

Our Take

The disruption fears seem overblown. The incumbent software firms are all pivoting to embedding AI in their workflows. Each engineer at these large firms is using AI to increase productivity. We see no reason a larger company with more resources cannot innovate as effectively as an AI-native startup. SaaS companies have a strong track record of innovating to keep big tech (Microsoft, Google, Amazon) out of their turf.

Vibe Coding

Markets are concerned that enterprises will build in-house AI software to avoid higher subscription costs. We don’t see this as a credible threat. Enterprises want someone accountable for failures, and they won’t replace third-party software licences that cost $20 to $100 per seat with an internal solution unless they have a large internal IT team (which is expensive). Also, most companies are not in the business of creating software. Software is a distraction for them.

Our Take

Enterprises will continue to outsource their software needs. Specialized software companies can produce software at much lower cost than an internal IT team (in most cases). Both sets of teams will be using the same AI agents or foundation models.

Even companies with their own foundation models, such as Anthropic, will prefer to license their models for a fee rather than develop, maintain, and be liable for outcomes for thousands of customers (which they would be if they sell Agents/Software directly).